ON THIS PAGE

Progress0%

Our Global Presence :

Consumer dissatisfaction with traditional banking models is steadily growing.

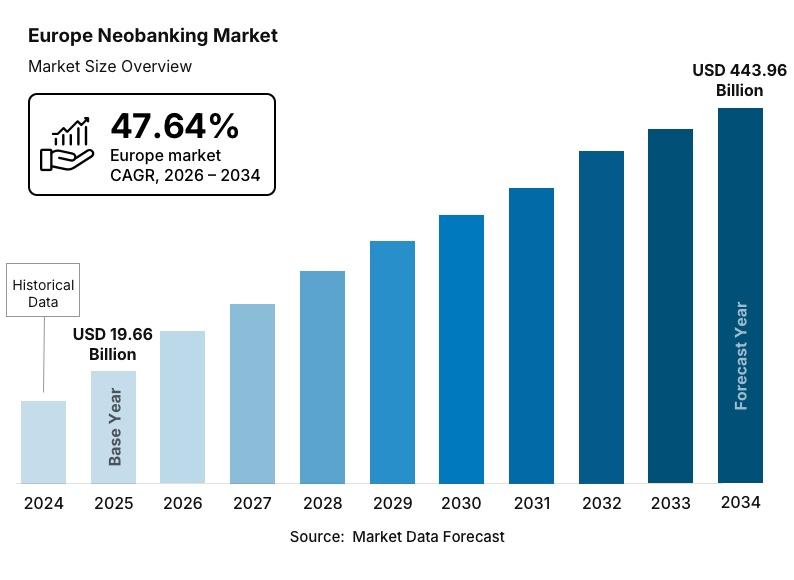

This is evident in the fact that the market size of the “digital alternatives” – neobanks – has been steadily growing as well. Valued at USD 13.32 billion in 2025, the Europe neobanking market has quickly reached USD 19.66 billion in 2026, and is now projected to reach USD 443.96 billion by 2034, according to Market Data Forecast.

The point here is that there’s a huge demand for neo-banking solutions. In that case, the market’s natural reaction is that there will also be a rise in the number of “solution providers” offering neobanking solutions.

Since building a quality neo banking solution is quite technical, most neo banking solution providers turn to white-label neo banking providers to expedite the process, and that’s where it gets tricky.

Here is the hard truth that most vendor brochures will not tell you: “not all white-label neobanking providers are built the same way.” If you didn’t know that and you chose the wrong partner, you could be in for a difficult stretch as you get exposed to regulatory risk, lack of support right when your customer base is scaling, and a whole bunch of other stuff that could go wrong.

The good news? Asking the right questions up front can save you years of costly course correction.

At Debut Infotech, we have spent years building, deploying, and supporting white-label neobanking solutions for clients across North America, Europe, and Southeast Asia. In that time, we have seen exactly where due diligence separates confident market entrants from those who just use any white-label neo banking platform in India.

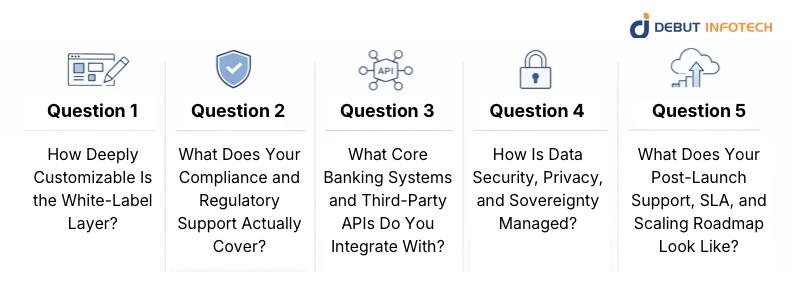

This guide distills that experience into the five most important questions you should ask any white label neo banking solution provider before you sign a contract — along with what a genuinely strong answer looks like and what red flags to watch for.

| Who Should Read This? This guide is built for fintech founders, CTOs, product leads, and banking executives who are actively evaluating white label, neobanking vendors. You should be asking the questions we’re about to discuss if you’re launching a challenger bank, building an embedded finance product, or modernizing a legacy banking stack. |

In neobanking, your brand IS your product. Customers can spot a generic, template-driven interface from a mile away, and if they peg your platform as one, they start losing trust and jumping to the competitor. Therefore, you need customization for authenticity.

But many “white label neo banking development services won’t tell you that. In fact, they will most likely offer you surface-level branding where you only have to swap the logo, change the color palette, and they call it done. Here’s a heads up, those aren’t the best choice for you.

The best choices for you should offer deep-layer customization that extends to user journeys, feature modules, notification logic, pricing rules, and more. The difference between these two approaches can determine whether your product genuinely stands apart in the market.

A credible provider should be able to walk you through customization across the following dimensions

Be wary of white label neo banking solutions with fixed demo environments and those that can’t demonstrate live customizations. Furthermore, if the provider says, “We’ll handle all design changes on our end,” you shouldn’t be too comfortable, because the idea of a “white label” solution is that you can customize things from your end.

Our white label neo banking platform is built on a decoupled front-end architecture, giving your design team full control over the UI layer without touching the core banking logic. From onboarding flows to account dashboards, every customer-facing element is modular, themeable, and independently deployable. We have delivered white label neo bank app development solutions ranging from a single-currency consumer app to a multi-product embedded finance platform. And we have done all of these from the same core engine, configured to look and feel entirely distinct.

Many first-time neobanking founders underestimate regulatory compliance, and most white label neo banking solution providers exploit this by misrepresenting key facts. They might just say “we are fully compliant,” but that is not enough, because the regulatory landscape for neobanking varies widely by jurisdiction.

For example, operating in the United States means navigating FinCEN requirements, BSA/AML obligations, and state-by-state money transmitter licensing. Europe brings PSD2, GDPR, and EBA guidelines into the picture. Southeast Asia has its own patchwork of central bank mandates. Therefore, a white label neo bank development company that is compliant in one region may leave you critically exposed in another.

However, beyond geography, you need clarity on two distinct compliance responsibilities: what the platform does by default, and what remains your obligation as the operator.

Look for specificity, not generality. A strong provider should be able to answer:

A vendor claiming to be “fully compliant” without specifying the jurisdictions and the specific versions of the regulations they comply with doesn’t look good.

Our platform ships with built-in KYC/AML workflows, transaction monitoring, suspicious activity reporting, and audit-ready logging. We work with clients to map their specific jurisdictional obligations and configure the compliance stack accordingly. For clients expanding across multiple markets, we have structured our compliance modules to be jurisdiction-aware.

A white-label neo banking platform needs to connect to payment rails, card issuance networks, banking-as-a-service providers, identity verification tools, credit scoring engines, accounting software, and much more. These integrations are quite important because they determine how your system scales as you add more users.

As such, integration limitations are one of the most common sources of technical debt in neobanking products. Many founders launch on a platform with tight integrations with a single BaaS partner or payment processor, only to discover months later that the platform cannot connect to a preferred partner, or that adding new integrations requires custom white-label neo bank development at high cost and with significant delay.

A technically mature provider should offer clarity on five integration dimensions:

A white-label neo bank development company that cannot share API documentation upfront, or whose integration list is vague and undated, is likely managing a fragile or proprietary stack. If every new integration requires a custom engagement with their white-label neo bank development team — and a new pricing conversation — that might be something to be wary of.

Our platform is built on an open API-first architecture with over 150 pre-built integration connectors spanning payment processing, card issuance, KYC/identity verification, credit decisioning, and accounting. As one of the best white-label neo banking platforms, we have active partnerships with leading BaaS providers and maintain clean integration layers with major banking cores. Our technical documentation is available during the evaluation phase so that you know what you’re dealing with from the outset.

You need to ask about data security because financial data is very sensitive. As such, a single breach can destroy customer trust overnight, trigger regulatory investigations, and produce liabilities that outlast the product itself.

When investigating a white-label neo banking solution’s data security and privacy, you need to distinctly consider the technical security architecture, data privacy compliance, and data sovereignty. Here’s what you should expect.

A strong response is characterised by clear, accurate standards that signify a codified approach to data security and privacy.

If a provider cannot produce current third-party security certifications, refuses to disclose data residency arrangements, or becomes vague when you ask about internal access controls, they might not be the right fit.

Our white label neo banking infrastructure supports multi-region deployment with configurable data residency, enabling clients to store customer data within the jurisdictions required by their regulatory environment. We operate in accordance with SOC 2 and PCI DSS standards and conduct annual third-party penetration testing. Every data access event within our platform is logged and auditable, and we maintain a documented, rehearsed incident response playbook with defined notification timelines.

Many white label neo bank development services feel strong during the sales process and the first few months of deployment, and then begin to fray precisely when they matter most, as the product scales and real-world complexity sets in. A provider that responds quickly to a pre-sales question may have a very different support posture for a client who has already paid and gone live.

The questions you ask about post-launch support, SLAs, and the provider’s own roadmap will reveal how they think about the long-term relationship versus the transaction.

Push for detail across three areas:

A provider who cannot articulate a clear SLA with measurable targets, or who becomes defensive when you ask about data portability and exit terms, is signaling that the post-contract relationship may not be a priority for them.

We operate on the principle that our clients’ growth is our growth. Every engagement includes a dedicated client success manager, tiered SLAs with defined response and resolution windows, and quarterly business reviews that align our roadmap to your evolving product needs. We also provide clients with structured data export capabilities from day one — because we believe you should never feel locked in.

Choosing a white label neo banking solution provider plays a major role in determining your product’s capabilities, regulatory posture, technical scalability, and customer experience for years to come.

The five questions we have outlined in this guide are designed to cut through the marketing surface and get to the operational truth of what a vendor can actually deliver:

At Debut Infotech, we welcome every one of these questions, because we have built our platform and our client relationships specifically to answer them well. Whether you are two weeks into your evaluation or six months into a painful experience with the wrong vendor, we are here to have an honest conversation about what the right solution looks like for your business.

A white label neo banking solution is a fully built digital banking platform — including account management, payments, card issuance, KYC/AML, and more — that is developed by a technology provider and licensed to businesses who can brand, configure, and deploy it as their own product. It eliminates the need to build core banking infrastructure from scratch, significantly reducing time-to-market and development cost.

With a mature provider and a clear product scope, a white label neobank can typically be launched in as little as 8 to 16 weeks. However, this timeline varies based on the complexity of regulatory requirements in your target market, the degree of customization needed, and how quickly your own licensing and banking partner arrangements are in place.

This depends on your jurisdiction and business model. In many markets, you can launch a neobanking product by partnering with a licensed bank or BaaS provider through a sponsor bank model — meaning you do not need your own banking license initially. A good white label provider should be able to advise you on the right licensing structure for your market and, in some cases, introduce you to appropriate banking partners.

Banking as a Service (BaaS) refers to the infrastructure layer — the licensed bank APIs and rails that power financial products. White label neobanking sits on top of BaaS infrastructure and refers specifically to a brandable, customer-facing product that is ready to deploy. White label neobanking solutions typically integrate with one or more BaaS providers to deliver their underlying financial functionality.

Total cost of ownership should include more than just the licensing fee. Consider implementation and integration costs, ongoing platform maintenance, compliance tooling, support tier pricing, transaction-based fees, and the cost of customization over time. Ask providers for a full breakdown over a two- to three-year horizon, and model both low- and high-growth scenarios to understand how per-transaction economics change at scale.

The best platforms are built on multi-tenant architecture, meaning a single platform can power multiple branded products with isolated data environments, distinct compliance configurations, and independent user experiences. This is particularly valuable for financial holding companies, BaaS providers, or operators who plan to serve multiple customer segments under different brand identities.

Debut Infotech is a global fintech product development company specializing in neobanking platforms, digital wallet solutions, and embedded finance products. With a client portfolio spanning North America, Europe, and Asia-Pacific, Debut Infotech combines deep regulatory knowledge, open API architecture, and a proven delivery model to help businesses launch financial products that are secure, scalable, and built to last.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

9001:2015

Quality Certified

ISO 27001

Security Certified

A+ Rating

Accredited Business

Certik

Security & Audit

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy