ON THIS PAGE

Progress0%

Our Global Presence :

The growth of the digital asset market has transformed the way people invest, trade, and conduct transactions worldwide. With the increasing popularity of cryptocurrencies as a financial instrument, regulation (and more specifically, taxation) has become a subject of concern for governments. The payment of cryptocurrency tax is no longer a possibility, particularly for individuals and businesses. It is an extremely significant factor in staying on the right track and avoiding costly penalties.

Although this significance has increased, taxation of cryptocurrency remains a puzzle to many. This is mostly because crypto transactions do not fit well into conventional tax systems. Trading, staking, or even paying with the crypto may lead to tax payments. Here, we are going to simplify cryptocurrency taxes explained in a straightforward, more practical manner: what is taxed, how they work, and how to effectively manage your tax responsibility.

Cryptocurrency taxation refers to the laws that govern the taxation of transactions involving digital assets by governments. Most jurisdictions do not regard cryptocurrencies as currency but as property or assets. It is construed that any crypto-to-crypto transactions will be taxed at the capital gains tax or the income tax.

To illustrate, receiving cryptocurrency and selling it later at a higher price will be counted as a capital gain. On the same note, when you receive crypto as payment for goods or services, it is considered income and is subject to taxation.

The Internal Revenue Service and other global regulators have indicated clearly that crypto transactions should be reported. Failure to do so will result in penalties or an audit.

To learn how to pay taxes on cryptocurrency, we have to learn the basic principles of crypto taxation. It has usually involved tracking transactions, calculating gains or income, and reporting them when one is filing taxes.

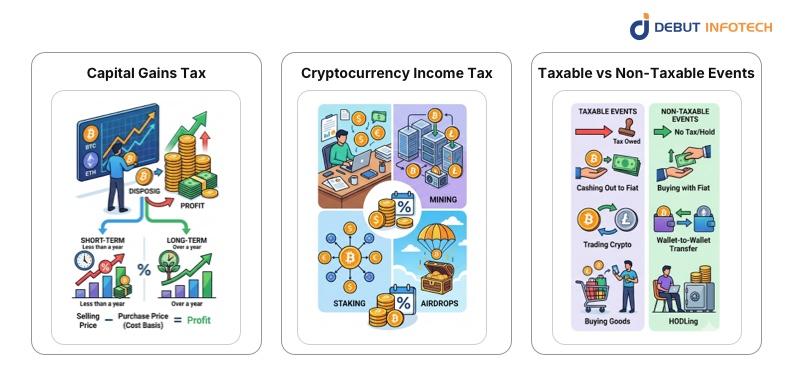

Capital gains tax is imposed when you sell or dispose of cryptocurrency at a profit.

The distinction between purchase price (cost basis) and selling price is the most important.

Not every crypto transaction qualifies as a capital gain. Some are considered income.

Examples include:

They are taxed in accordance with their fair market value when they are received.

Understanding what events are taxable and which events are not taxable is important.

Taxable events include:

Non-taxable events include:

Not all crypto activity is taxed equally. The type of transaction determines how it is taxed.

1. Trading Cryptocurrency: Swapping or exchanging one cryptocurrency for another is seen as a taxable event. The transaction is still subject to tax even if you do not convert the crypto to fiat.

For example, exchanging Bitcoin for Ethereum results in a taxable gain or loss based on the difference in value.

2. Selling Cryptocurrency: The most frequent type of taxable event is to sell crypto in fiat currency. Capital gains tax is imposed on the profit made.

3. Spending Cryptocurrency: There is also taxation of the use of crypto to buy goods or services. This is because the transaction is considered a disposal of the asset.

4. Earning Cryptocurrency: Any crypto earned through freelancing, salaries, or business transactions is considered taxable income.

It is particularly applicable to any business that incorporates a crypto payment gateway, as transactions must be registered and reported correctly.

5. Mining and Staking Rewards: Mining and staking rewards are treated as income at the time they are received. If you later sell these assets, you may also incur capital gains tax.

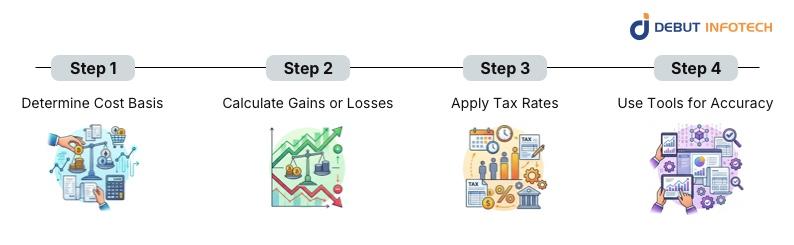

Computing crypto taxes requires closely monitoring all activities. It may be a complicated process, particularly for frequent traders.

The cost basis is the original value of your crypto when you acquired it. This includes:

Subtract the cost basis from the selling price.

Apply the appropriate tax rate based on:

Many users rely on a cryptocurrency tax calculator to automate this process. These tools help track transactions, calculate gains, and generate tax reports.

Crypto taxation is not always straightforward. There are several challenges that users face.

1. Tracking Transactions Across Wallets: Users often store assets in multiple wallets, including:

Tracking transactions across these systems can be difficult.

2. High Trading Frequency: Frequent traders may execute hundreds of transactions. This makes manual tracking nearly impossible.

3. Modifying Regulations: Crypto tax laws are in their formative stage. The rules vary by country and are frequently updated.

4. Ignorance: This is due to the fact that the lack of awareness has made many users unaware that some events, such as the swapping of tokens, are taxable.

Best practices need to be observed to ensure that one remains in line and eliminates stress.

A large number of individuals search for ways to avoid capital gains tax on cryptocurrency. Although it is not always possible to completely avoid taxes, there are legal methods by which you can decrease the amount of taxes.

Some common approaches include:

Nevertheless, legal principles should be observed and risky behaviors avoided.

With the rise in crypto usage, infrastructure should be considered a central part of tax reporting.

Some common features that are utilized with businesses related to a crypto development company may include:

Some of the solutions, such as the crypto wallet development services and white label crypto wallet, can be integrated with features of tracking, which users can find when it comes to reporting their taxes.

Although fundamental tax compliance is necessary, more advanced investors and companies seek opportunities to address their tax payments efficiently. Learning sophisticated techniques will enable you to do this without breaking the law and bearing a heavy load.

Tax-loss harvesting is one of the most widespread ones. This includes selling underperforming assets to incur a loss, which can then be offset by gains on profitable trades. With active traders, the strategy can save a lot of tax in general.

The other strategy that is worthwhile is long-term holding of assets. Most jurisdictions receive lower rates on long-term holdings than on short-term trades. This will motivate investors to become more strategic and long-term instead of trading intensively.

Asset and jurisdiction diversification may also be a factor. There are also investors exploring areas with more favorable tax policies, but this must be done with proper planning and adherence to local laws.

Diversification across assets and jurisdictions can also play a role. Some investors explore regions with more favorable tax policies, although this requires careful planning and compliance with local regulations.

Cryptocurrency tax is not limited to individual investors. Businesses that receive, save, or trade crypto are also obliged to pay taxes.

Companies that incorporate a crypto payment gateway will have to trace all the transactions correctly. Every cryptocurrency transaction is considered income based on its fair market value when received. This implies that companies will be required to keep comprehensive accounting and reporting records.

Also, companies that use solutions such as centralized wallet systems or create their wallets with crypto wallet development services must ensure they have appropriate tracking systems. This is particularly necessary in companies operating at scale, where transaction volumes may be very large.

Startups in crypto, including those that deal with a crypto development company, tend to incorporate compliance features into their platforms. These can be automated reporting software, transaction records, and compatibility with tax software.

Among the most difficult issues in cryptocurrency taxation is that laws differ across countries.

In certain nations, crypto is treated as property, with every transaction subject to tax. In others, some transactions can be left tax-free or taxed differently. For example, certain jurisdictions provide tax exemptions for long-term holdings or minor transactions.

Governments like HM Revenue and Customs and the Australian Taxation Office have issued detailed guidance on the taxability of crypto, underscoring the growing significance of digital assets in the world of finance.

To international companies and investors, this may make compliance a complicated affair. One must be knowledgeable of the regulations in the various jurisdictions in which you are or have properties.

Cryptocurrency taxes can be confusing even to seasoned users. These are some of the typical mistakes that you can avoid to evade penalties and audits.

Omission of reporting all transactions is one of the key errors. Most users believe that conversion to fiat is the only taxable activity, but, as mentioned above, a crypto-to-crypto trade is also a taxable event.

The other problem is the incorrect cost basis calculation. Gains or losses cannot be determined accurately without proper records. It may result in underpaying or overreporting taxes.

Other users even overlook minor transactions, thinking that they are not important. Nevertheless, tax authorities may still demand full disclosure, irrespective of transaction volume.

Lastly, manual tracking is unreliable and may lead to errors. One should use such tools as a cryptocurrency tax calculator to be precise and efficient.

The choice of wallet is also important in determining how easy it is to manage your crypto taxes.

Users tend to keep their assets in a number of wallets, such as decentralized wallets and custodials. All the wallets document transactions differently, which complicates tracking.

It can be made easy by using some well-designed wallets that have built-in tracking features. The majority of the best crypto wallets have transaction histories, export features, and support tax software.

Companies investing in crypto wallet solutions, such as white-label or more advanced services like Ordinal Wallet Development, can incorporate tax-friendly features from the very beginning of their development. This enhances the level of transparency as well as compliance difficulties among users.

The future of cryptocurrency tax is probably to get more organized and technological. Governments are also funding mechanisms to monitor blockchain transactions more efficiently, suggesting that compliance requirements will be tightened in the future.

Automation of tax reporting is a significant trend. Exchanges and platforms may be compelled to provide standardized reports to users and tax authorities. This will minimize manual work but enhance transparency.

The next trend is the added value of tax features to blockchain platforms. The use of compliance tools in an ecosystem is already being investigated by projects created by the top cryptocurrency companies.

It is also likely that we will see more transparent global frameworks as regulators strive to harmonize crypto taxes. This will facilitate easier compliance for businesses that are working in various regions.

For businesses, it is up to the enterprise to remain within the boundaries of crypto taxation.

First, there is a need to develop systems that support proper record-keeping. This involves monitoring all the transacted information, the historical information, and providing easy access to the reports.

Second, compliance tools can be incorporated into the development process, thereby saving time and costs in the long term. Such features as automated reporting and audit trails can be implemented by businesses that cooperate with an experienced crypto development company.

Third, it is necessary to stay abreast of regulatory changes. Cryptocurrency regulations change rapidly, and companies must adjust to avoid punishment.

Lastly, collaboration with specialists, both technical and financial, is a guarantee that your platform and activities do not violate any rules and remain efficient.

People interested in the digital asset sector, whether as individual investors or businesses, should understand cryptocurrency taxes. Due to the increased use of crypto, governments increasingly require greater levels of transparency and compliance.

Trading, staking, payments, and wallet transfers all involve various tax requirements. Understanding what is taxed and calculating it correctly can help you avoid the expensive errors and fees.

Simultaneously, the development of crypto infrastructure, such as wallets and development platforms, is simplifying tax management. With the right tools and by working with partners who have been in the business, individuals and businesses can make compliance easier and focus on growth.

With regulations changing regularly, it will be important to stay up to date and be proactive. When handled correctly, crypto taxation can be less burdensome and become a more organized part of your financial strategy.

No, not all transactions are taxable. Buying cryptocurrency with fiat or transferring assets between your own wallets is generally not subject to tax. However, selling, trading, or using crypto for purchases is considered a taxable event under most cryptocurrency tax regulations.

Cryptocurrency gains are usually taxed as capital gains. The tax is calculated based on the difference between the purchase price (cost basis) and the selling price. The rate may vary depending on how long you hold the asset and your local tax laws.

No, simply holding cryptocurrency does not trigger a tax obligation. Taxes only apply when you dispose of the asset, such as selling, trading, or using it for payments.

Yes, trading one cryptocurrency for another is considered a taxable event in most jurisdictions. Even if no fiat currency is involved, the transaction must be reported as part of your cryptocurrency tax filings.

You can calculate your taxes by tracking your cost basis, transaction history, and gains or losses. Many users rely on a cryptocurrency tax calculator to automate this process and reduce errors.

Failing to report crypto taxes can lead to penalties, fines, or audits by tax authorities. Agencies like the Internal Revenue Service actively monitor crypto transactions and enforce compliance.

Yes, you can reduce your tax burden through legal strategies such as holding assets long-term, offsetting gains with losses, and maintaining accurate records. Consulting a tax professional can also help optimize your strategy while staying compliant.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy