ON THIS PAGE

Progress0%

Our Global Presence :

Cryptocurrency mining is the process of verifying transactions on a blockchain and introducing new digital coins into circulation. It relies on powerful computers solving cryptographic puzzles to secure decentralized networks such as Bitcoin. The scale of cryptocurrency mining has grown significantly as blockchain adoption has increased.

According to a report from World Data, the Bitcoin network’s total mining hash rate peaked at 943 exahashes per second (EH/s) in 2025, demonstrating the immense computing power required to secure the network. At the same time, mining infrastructure consumes substantial energy, with global Bitcoin mining estimated to use about 131 terawatt-hours (TWh) of electricity annually. These figures highlight the technological intensity behind modern blockchain systems.

Understanding cryptocurrency mining involves exploring how the process works, the tools miners use, the various mining methods available, and the benefits and risks of participating in this decentralised verification system. This guide will equip you with this crucial information.

Cryptocurrency mining is the process of validating transactions and adding them to a blockchain network. It relies on computing power to solve mathematical problems that confirm the authenticity of digital transactions. Once verified, those transactions become permanent entries on the blockchain ledger.

Mining also introduces new cryptocurrency into circulation, which is why it plays a central role in networks like Bitcoin. The process combines cryptography, distributed computing, and economic incentives. Miners contribute computational resources to maintain the network and receive rewards in return.

Without mining or an equivalent consensus mechanism, many blockchain networks would struggle to maintain trust, transparency, and data integrity across decentralized systems.

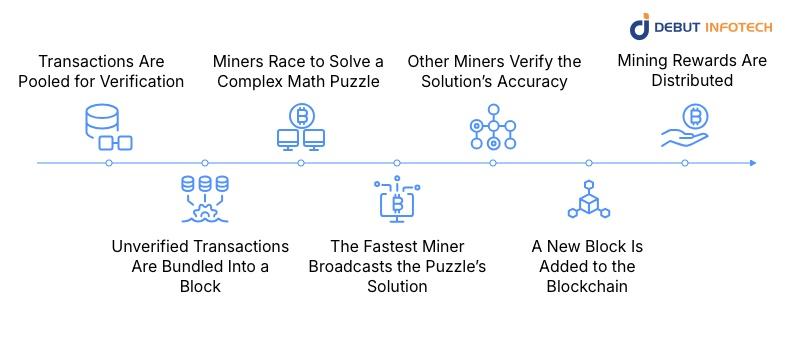

Cryptocurrency mining follows a structured verification process designed to maintain trust across a decentralized network. Each step ensures that transactions are legitimate before they are added to the blockchain. Miners compete to validate transaction blocks using computing power. The process balances security, decentralization, and transparency while rewarding participants who contribute computational resources.

Every time a user sends cryptocurrency, the transaction enters a network queue known as the mempool. These transactions remain unconfirmed until miners select them for validation.

Mining nodes constantly monitor the pool and choose transactions based on factors such as fees and network rules. Pooling transactions in this manner ensures that only legitimate transactions move forward in the verification process.

Miners group several pending transactions into a single data structure called a block. Each block contains transaction records, timestamps, and a reference to the previous block in the chain. This linking mechanism forms the blockchain structure.

Organizing transactions into blocks improves efficiency and enables the network to process many transactions simultaneously while maintaining an accurate and tamper-resistant ledger.

Once a block is prepared, miners begin solving a cryptographic puzzle linked to that block. The puzzle requires finding a hash value that meets strict conditions set by the network.

Solving it requires substantial computational effort rather than advanced mathematical insight. Miners continuously run calculations until one participant finds a valid hash that satisfies the network’s difficulty requirements.

The miner who successfully discovers the correct hash broadcasts the solution to the entire network. This announcement allows other nodes to review the work and verify that the block was created in accordance with the protocol rules.

Broadcasting the result ensures transparency and prevents a single participant from controlling transaction validation without network approval.

Other miners independently check the solution to confirm that it meets the network’s requirements. Verification takes far less computing power than solving the puzzle itself. This asymmetry allows the network to quickly validate legitimate blocks while making fraudulent attempts impractical. Only when consensus is reached does the network accept the newly mined block.

After successful verification, the block becomes part of the blockchain. The ledger updates across all participating nodes, creating a synchronized record of transactions.

Each block strengthens the chain by linking to the previous block through cryptographic hashes. This structure protects the ledger against tampering because altering any block would require recalculating every subsequent block.

The miner responsible for solving the block receives a reward from the network. This reward usually includes newly minted cryptocurrency and transaction fees from the block’s transactions.

Rewards encourage miners to contribute computational resources to the network. The incentive structure sustains participation and ensures the continued operation of decentralized blockchain systems.

Mining cryptocurrency requires specialized tools that support transaction validation and cryptographic calculations. These tools allow miners to connect to blockchain networks, manage rewards, and perform the computational work required for mining.

A cryptocurrency wallet stores the rewards earned from mining. It holds private keys that allow miners to access and transfer their digital assets. Wallets may exist as software applications, hardware devices, or cloud-based services. Selecting a secure centralized or decentralized wallet is an important step because it protects mining earnings from unauthorized access.

Mining software connects hardware to the blockchain network and coordinates the mining process. The software receives transaction data, performs hashing operations, and communicates results with other network nodes. Many mining applications also allow miners to monitor performance, adjust configuration settings, and connect to mining pools for collaborative mining.

Mining hardware performs the computational work required to solve cryptographic puzzles. The most common hardware options include specialized ASIC machines, graphics processing units (GPUs), and, in some cases, standard CPUs. Hardware selection influences mining efficiency, electricity consumption, and potential profitability. Choosing appropriate hardware remains a critical decision for anyone entering cryptocurrency mining.

Miner’s Reality: The Power & Noise Factor

A single ASIC miner (like the Antminer S21) produces roughly 75–80 dB of noise—comparable to a loud vacuum cleaner running 24/7. Most residential spaces cannot handle this without dedicated soundproofing.

Additionally, these machines require a 220V–240V outlet; plugging them into a standard home socket will likely trip your circuit breaker.

Cryptocurrency mining can take several forms depending on the hardware used, the network design, and the level of participation required. Each mining type offers different levels of efficiency, accessibility, and cost.

Application-Specific Integrated Circuit (ASIC) mining uses specialized hardware designed specifically for mining certain cryptocurrencies. ASIC machines deliver extremely high computational performance compared to general-purpose hardware. They are widely used in large mining operations because they solve hashing puzzles faster and more efficiently than CPUs or GPUs.

CPU mining relies on the central processing unit of a standard computer to perform hashing calculations. This method was common during the early years of cryptocurrency when mining difficulty was low. Modern blockchain networks typically require far more computing power, reducing the practicality of CPU mining for many popular cryptocurrencies.

Mining pools allow multiple miners to combine their computational resources and share rewards. Participants contribute hashing power to the pool and receive payouts based on their contribution. Pools help smaller miners compete with large operations by providing more consistent reward distribution and reducing the unpredictability associated with solo mining.

Cloud mining provides access to remote mining hardware through online services. Instead of purchasing equipment, users rent computing power from a provider. The provider manages hardware maintenance and electricity costs. Cloud mining lowers the technical barrier to entry. However, participants must carefully evaluate service providers to avoid unreliable or fraudulent platforms.

Quick-Reference: Choosing Your Mining Path

| Mining Type | Entry Cost | Technical Difficulty | Best For | Typical Hardware |

| ASIC (Pool) | High ($2,000+) | Moderate / Hard | Serious ROI & Bitcoin | Bitmain Antminer, Whatsminer |

| GPU Mining | Moderate ($800+) | Hard (Setup-heavy) | Altcoins & Hobbyists | NVIDIA RTX 40-series, AMD Radion |

| Cloud Mining | Low ($50+) | Easy | Beginners / Passive | None (Rented Power) |

| CPU Mining | Near Zero | Very Easy | Learning Only | Standard PC / Laptop |

Cryptocurrency mining contributes directly to the functionality, reliability, and growth of blockchain networks. By validating transactions and maintaining decentralized records, mining supports the operational structure that allows cryptocurrencies to exist without centralized authorities.

Beyond technical maintenance, mining also introduces economic incentives that encourage global participation in blockchain ecosystems.

Mining allows blockchain networks to process and confirm transactions without relying on a central authority. Miners verify transaction data, package it into blocks, and add those blocks to the distributed ledger. This process ensures that the blockchain continues to function reliably while maintaining transparency and trust among participants across the decentralized network.

Mining introduces new cryptocurrency into circulation through a structured reward system tied to the creation of blocks. Miners receive newly minted coins and transaction fees for validating blocks. This mechanism distributes digital assets across the network while encouraging continued participation from miners who provide the computing power necessary to sustain blockchain operations.

Cryptocurrency mining strengthens blockchain security by requiring significant computational effort to alter transaction records. Each new block becomes cryptographically linked to the previous one, making tampering extremely difficult.

To manipulate the blockchain, a malicious actor would need enormous computing resources to recalculate multiple blocks across the network simultaneously.

Cryptocurrency mining generates financial opportunities for individuals, businesses, and technology providers participating in blockchain ecosystems. They also generate financial opportunities for companies offering crypto wallet development services.

Miners earn rewards for contributing computing power, while related industries benefit from growing demand for specialized hardware, energy infrastructure, and data center services. These activities contribute to a broader digital economy built around decentralized technologies.

Despite its benefits, cryptocurrency mining also involves several operational and financial risks. Understanding these challenges helps participants make informed decisions before investing in mining infrastructure.

Government policies related to cryptocurrency mining vary across jurisdictions. Some countries support mining operations, while others impose restrictions or licensing requirements. Regulatory changes can affect mining profitability, operational costs, and the long-term viability of mining businesses.

Cryptocurrency prices fluctuate frequently. Mining profitability depends heavily on the market value of the mined asset. When prices decline, mining revenue may not cover electricity and equipment costs. Miners and top cryptocurrency companies often closely monitor market trends to assess operational sustainability.

Mining requires large amounts of electricity because computational hardware runs continuously. High energy consumption raises operational costs and has sparked debates about environmental impact. Many mining operations now explore renewable energy sources to reduce both costs and environmental concerns.

Mining systems can become targets for cyberattacks, malware, and unauthorized access. Attackers may attempt to hijack computing power or steal cryptocurrency rewards. Secure network configurations, updated software or centralized wallet, and strong access controls reduce these risks.

Mining involves technical setup, hardware configuration, and network integration. Beginners may face challenges with system optimization, cooling requirements, and managing mining software. Learning these technical aspects requires time, experimentation, and continuous monitoring of mining performance.

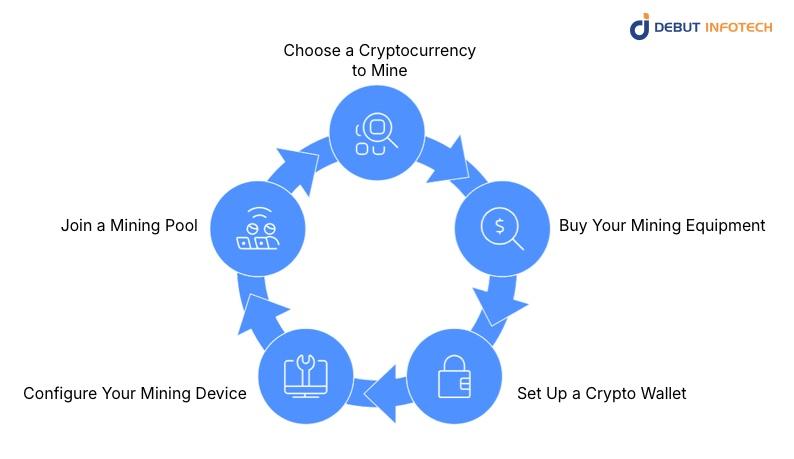

Starting cryptocurrency mining requires careful preparation, technical setup, and a clear understanding of operational costs. Mining involves hardware investment, software configuration, and network participation. Following structured steps helps new miners establish a stable setup, manage rewards securely, and participate effectively in validating blockchain transactions.

Selecting the right cryptocurrency determines the hardware requirements, mining difficulty, and potential profitability of your operation. Research factors such as network hash rate, block rewards, transaction fees, and mining algorithms.

Some cryptocurrencies require ASIC hardware, while others remain compatible with GPUs. A careful evaluation helps miners identify networks where participation remains feasible and financially sustainable.

Mining hardware performs the calculations needed to validate blockchain transactions. Many miners choose ASIC machines for their efficiency in solving hashing puzzles, though GPU-based rigs still support certain cryptocurrencies.

Equipment selection should consider processing power, electricity consumption, cooling requirements, and durability. Investing in reliable hardware helps maintain stable mining performance and reduce unexpected downtime.

Miner’s Reality: Thermal & Humidity Challenges

The Cooling Factor

In many parts of the US, ambient temperature fluctuations can be a miner’s biggest enemy. It is a common mistake to assume a standard HVAC system can handle a mining rig; in reality, a single ASIC puts out as much heat as a small furnace.

To maintain peak profitability, you must implement a “High-Volume Airflow” strategy. This involves industrial exhaust fans that swap the air in the room every 30–60 seconds. Without this, your hardware will “thermal throttle”—automatically slowing down to prevent melting—which kills your ROI.

A cryptocurrency wallet stores the digital assets earned from mining activities. The wallet generates private keys that provide secure access to mining rewards and transaction capabilities.

Miners often choose hardware wallets or reputable software wallets for enhanced security. Proper wallet configuration protects earnings while ensuring that rewards from mining pools or blocks reach the correct destination.

Mining devices must be configured with the appropriate software before they begin processing blockchain transactions. This setup involves installing mining software, entering wallet addresses, and selecting the correct mining algorithm.

Adjusting system settings, monitoring temperatures, and optimising power usage help maintain efficient operation while reducing the risk of hardware damage during continuous mining.

Joining a mining pool allows miners to combine their computing power with others’ to increase their chances of successfully mining blocks. The pool coordinates mining activity and distributes rewards among members based on their contributed hashing power.

Pool participation provides more predictable earnings than solo mining, particularly for miners with limited hardware capacity.

Cryptocurrency mining can remain profitable under the right conditions, though the economics have become more complex. Profitability depends on hardware efficiency, electricity costs, network difficulty, and cryptocurrency prices. Large-scale mining operations benefit from economies of scale, access to cheaper electricity, and optimized infrastructure.

Individual miners often evaluate profitability using mining calculators that estimate potential returns based on power consumption and hardware performance. These tools provide guidance, though real earnings still depend on market fluctuations and mining difficulty adjustments.

Mining continues to play a fundamental role in maintaining blockchain networks. While competition has increased, opportunities still exist for participants who plan carefully, control operational costs, and choose suitable mining strategies.

Strategic planning, efficient hardware, and stable energy sources significantly improve the chances of achieving sustainable mining returns.

Miner’s Reality: The Maintenance Grind

Profit isn’t just “Revenue minus Electricity.” You must factor in downtime. Dust is the enemy of hash rate; plan to deep-clean your fans and heat sinks with compressed air every 3 to 6 months to maintain peak efficiency.

Cryptocurrency mining remains a core mechanism that keeps blockchain networks secure, transparent, and decentralized. Through computational verification, miners confirm transactions, add blocks to the ledger, and earn rewards that sustain network participation. The process involves specialized tools, different mining methods, and careful management of operational costs.

While profitability depends on factors such as electricity prices, hardware efficiency, and market conditions, cryptocurrency mining continues to support the long-term reliability and expansion of blockchain ecosystems.

Businesses exploring blockchain solutions often require expert technical support. As a top-tier crypto development company, Debut Infotech develops secure blockchain platforms, crypto applications, and enterprise solutions that integrate technologies such as cryptocurrency mining infrastructure, smart contracts, and decentralised systems.

Our engineering team helps organizations design scalable blockchain products that align with evolving digital finance and Web3 innovations.

Yes, crypto mining can make money, but the margins depend on several factors. Electricity costs, mining hardware, and the current price of the cryptocurrency all matter. Large mining operations often earn more because they operate more efficiently. For individuals, profits vary and can be fairly modest.

Crypto mining itself is legal in many countries, though regulations vary by country. Some governments restrict or ban it due to energy concerns or financial policies. Others allow it with certain rules. Anyone planning to mine should check local laws before setting up equipment.

Yes, a regular person can mine crypto, though it’s no longer as simple as it once was. Early miners could use standard computers. Today, most profitable mining requires specialised machinery and a stable power supply. Some people still mine at home, but large mining farms dominate the industry.

No, crypto mining is not stealing when it is done properly. Miners simply use computing power to validate transactions and secure the blockchain network. Problems arise when someone secretly installs mining software on another person’s computer. That practice, known as cryptojacking, is illegal.

Mining a full Bitcoin alone can take years with a single machine. The network is competitive, and difficulty levels are high. Most miners join mining pools, where rewards are shared among participants. In that setup, miners earn small fractions of Bitcoin regularly rather than waiting for a full coin.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

9001:2015

Quality Certified

ISO 27001

Security Certified

A+ Rating

Accredited Business

Certik

Security & Audit

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy