ON THIS PAGE

Progress0%

Our Global Presence :

Crypto exchange infrastructure is an interconnected system where the order book, matching engine, internal ledger, wallet infrastructure, liquidity, and compliance layers must work together to process trades accurately.

The matching engine determines execution quality, using price-time priority, deterministic processing, and atomic updates to deliver reliable trade execution and maintain ledger consistency.

Liquidity directly impacts trading performance, influencing spreads, slippage, execution speed, and user trust through market makers, liquidity providers, and sufficient order book depth.

Wallets, custody, and internal ledgers serve distinct roles, with wallets managing on-chain assets, custody protecting private keys, and the ledger maintaining accurate balances and settlement records.

Choosing between CEX, DEX, P2P, Hybrid, or OTC models depends on business goals, as each architecture introduces different requirements for custody, smart contracts, escrow, compliance, and backend infrastructure.

Poor exchange architecture creates operational and financial risk, including ledger mismatches, wallet security gaps, execution failures, and liquidity issues that can damage platform reliability and user confidence.

Infrastructure readiness should be validated before development begins, ensuring trading workflows, liquidity strategy, custody, settlement, KYC/AML, and security controls are clearly defined to reduce implementation risk and unexpected costs.

When a user clicks “Buy BTC” or “Sell ETH,” the trade may look instant on the screen. But behind that single action, several exchange systems start working together. This is where understanding how cryptocurrency exchanges work becomes practical, especially if you are planning to build or buy one.

First, the platform confirms the user’s identity and session through account authentication. Then it checks whether the user has enough available balance, whether the trade meets platform rules, and whether any risk controls should block or flag the order.

Once the order is validated, it moves toward the order book, where open buy and sell orders are organized by price and quantity. The matching engine then looks for a compatible counterparty. For instance, when a user sends a market order to purchase BTC, the engine will search for the best available sell orders with matching prices and available liquidity.

Once executed, the exchange will provisionally update its internal ledger, calculate trading fees, refresh market data and record the asset balances. The wallet and custody layer still remains responsible for actual fund control, asset storage, withdrawals, and deposits.

This article explains how order books, matching engines, liquidity, wallets, custody, ledgers, and backend architecture work together behind the exchange interface.

The crypto exchange working mechanism is not just a user clicking “buy” or “sell.” Behind that simple action is a connected flow of identity checks, payment rails, wallet systems, internal ledgers, order validation, matching engines, market data services, and settlement processes.

The trading journey starts with account creation. Depending on the exchange’s rules, the platform may check the user’s identity, screen for sanctions exposure, verify the device, review account status, and assign trading permissions.

This is where the exchange decides what the user can access. A verified retail user, institutional trader, restricted-location user, or higher-risk account may have different deposit limits, trading limits, withdrawal rules, and review requirements.

Once the account is active, the user can deposit funds.

For fiat deposits, the exchange connects to banks, card networks, payment gateways, or local payment rails. For crypto deposits, the wallet system watches the blockchain and confirms the transaction after the required number of network confirmations.

The user’s balance is credited only after the deposit is accepted and confirmed.

3. Ledger Balance Update

On a centralized exchange, the user’s tradable balance is usually recorded in an internal ledger. The actual crypto may be stored in hot, warm, or cold wallets, but the user trades against the balance shown in the exchange backend.

The ledger records available balance, locked balance, fees, trades, deposits, withdrawals, and settlement history. This makes it the main record for what each user owns and what they can trade.

After the balance is available, the user can place a buy or sell order. The order contains details such as trading pair, quantity, price, order type, and execution rules.

For example, a limit order to buy 1 ETH at 3,000 USDT should only execute at 3,000 USDT or below.

Before the order enters the market, the system checks whether it is allowed. It confirms that the user has enough balance, the order format is valid, the account is not restricted, the trading pair is active, and risk or compliance rules are not breached.

These checks help prevent overdrafts, invalid orders, blocked-account trades, and exposure beyond approved limits.

After validation, the order is sent to the order book or matched immediately.

A limit order may wait until another trader accepts the price. A market order usually executes against existing orders at the best available prices. The matching engine pairs buy and sell orders using rules such as price priority and time priority.

When the trade is executed, the ledger updates both sides. The buyer receives the crypto asset, the seller receives the quote currency, and the exchange records applicable fees.

This internal settlement is why centralized exchanges can process trades quickly without posting every trade directly to the blockchain.

After execution, market data services update the trading screen, mobile app, charts, order book, and APIs. Users can then see the latest price, trade volume, order book depth, candlestick changes, and trade history.

A withdrawal is not the same as trade settlement. When a user withdraws crypto, the wallet or custody system signs and broadcasts an on-chain transaction.

In simple terms, trading happens inside the exchange ledger, while blockchain settlement mainly happens when crypto enters or leaves the platform.

A crypto exchange is not a single application. It is a collection of related systems that need to operate in a real-time manner. If you’re looking to get a good explanation of a crypto exchange platform from an infrastructure perspective, the table below outlines the essential systems that run behind the user-facing product.

| Core System | What It Does | Why It Matters | Practical Decision Check |

| User Interface | Lets users view markets, place orders, track balances, and manage accounts. | Good UX improves adoption, but it does not execute trades by itself | Is the interface connected to real-time balances, order status, and market data? |

| API Gateway | Routes web, mobile, admin, and institutional requests to backend services. | Controls access, traffic flow, authentication, and service communication | Can it handle high request volume without exposing backend systems? |

| Order Book | Stores active buy and sell orders by trading pair. | Enables price discovery, visible market depth, and liquidity assessment | Does it update instantly when orders are placed, matched, or cancelled? |

| Matching Engine | Matches compatible orders based on exchange rules. | Determines trade speed, fairness, accuracy, and execution priority | Are matching rules clearly defined and tested under load? |

| Internal Ledger | Tracks balances, locked funds, trades, fees, and settlement entries. | Prevents balance errors, double spending, and accounting inconsistencies | Is every trade recorded before balances are released or updated? |

| Wallet Infrastructure | Manages deposits, withdrawals, addresses, hot wallets, and cold storage | Protects digital assets and connects the platform to blockchains | Are withdrawal approvals, custody rules, and wallet limits clearly controlled? |

| Liquidity System | Connects market makers, liquidity providers, aggregators, and internal pools | Affects spreads, slippage, and whether users can trade smoothly | Will liquidity be internal, external, market-maker supported, or hybrid? |

| Market Data Service | Publishes live prices, order book changes, and trade updates | Powers charts, APIs, bots, and institutional trading feeds | Is the data fast, consistent, and available across all user channels? |

| Risk Engine | Applies limits, price bands, fraud checks, and liquidation logic where needed | Protects the exchange from abuse, abnormal trades, and exposure | What rules stop suspicious trading before damage occurs? |

| Compliance Layer | Handles KYC, AML, monitoring, reporting, and admin review workflows | Supports regulated operations and reduces legal and financial risk | Can compliance teams review users, transactions, and alerts efficiently? |

| Admin Console | Gives operators control over users, assets, trading pairs, fees, and risk settings | Essential for daily operations, investigations, and incident response | Can operators act quickly without engineering support for every change? |

The important point to remember is that exchange performance is not just about the presence of these systems, it’s about their interactions. A robust build should be in place that links trading, custody, liquidity, compliance and operations together with solid backend architecture. When assessing a vendor or internal build plan, consider the quality of these connections, audit trail, and platform behaviour on high volume trading and operational incidents.

An order book is one of the core systems that helps a crypto exchange discover price in real time. It shows open buy and sell orders for a particular trading pair like BTC/USDT, and arranges them based on price level and volume.

Buy orders are called bids. Sell orders are called asks. The highest bid is the best price a buyer is willing to pay, and the lowest ask is the best price that a seller is willing to accept. The difference between these two prices is called the spread.

This spread gives traders a quick view of trading friction. When the spread is tight, this indicates a market where there are sufficient buyers and sellers near the current market price. A wider spread can indicate poor liquidity, increased cost of execution or increased risk of slippage.

Price discovery happens because the order book reflects live market intent. Every new limit order, market order, cancellation, and executed trade changes the available supply and demand at different price levels. The matching engine uses this order book to match compatible buyers and sellers based on the exchange’s execution rules.

The relationship between order types is important. A limit order provides liquidity when it is on the order book and waiting to be executed. For instance, a trader may place a buy limit order at $69,950. That order does not execute immediately if the market is higher, but it becomes available liquidity for future sellers.

A market order does the opposite. It consumes liquidity by executing against existing orders already placed in the book. If a trader places a market buy order, the system fills it against the lowest available asks first. Once those asks are filled, the order moves to the next price level until the full quantity is executed.

This is where market depth matters. If there is enough volume at or near the best ask, the trade may execute with little price movement. But if the order is large and available volume is thin, it may move through several ask levels. That difference between the expected price and the final average execution price is called slippage.

For founders and product teams evaluating crypto exchange development services, the order book should not be treated as a simple table of prices. It is a real-time liquidity layer that connects trader activity, matching logic, market depth, spread behavior, and execution quality. If it is poorly designed, the exchange may look functional on the surface but fail when trading activity increases.

A matching engine is the system that makes trading happen inside a crypto exchange. It accepts valid buy and sell orders, matches them with the orderbook, determines which orders can be executed and notifies the other backend applications.

It operates between the order book, ledger, risk layer and the market data pipeline. If it is not included, the exchange might provide prices and receive orders but not be able to execute orders in a reliable and controlled manner.

A crypto exchange is not a single application. It’s a group of interrelated systems that collaborate.

The matching engine links three crucial components of that system:

| System | Role in the Trading Flow |

| Order Book | Stores open buy and sell orders by trading pair |

| Matching Engine | Matches compatible orders and creates trade executions |

| Ledger | Updates balances, fees, locked funds, and settlement records |

This relationship is important. The order book shows available market interest. The matching engine decides when that interest becomes a trade. The ledger records the financial result of that trade.

When a trader enters an order, the matching engine doesn’t just look at the order as a “buy” or “sell” order. It processes the order through a controlled sequence.

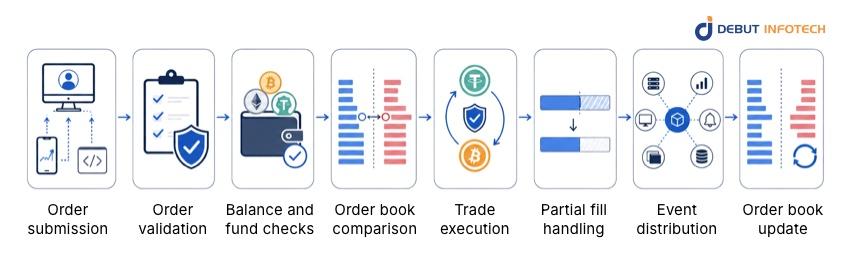

A typical flow looks like this:

1. Order submission

The user submits an order via the web interface, mobile application, API or institutional trading connection.

2. Order validation

The system checks the trading pair, order type, price, quantity, user status, and account permissions.

3. Balance and fund checks

The platform confirms that the user has enough available balance. For buy orders, quote currency may be locked. For sell orders, the asset being sold may be locked.

4. Order book comparison

The matching engine checks the incoming order against the opposite side of the order book.

5. Trade execution

If prices are compatible, the engine executes the trade.

6. Partial fill handling

If only part of the order can be matched, the engine fills the available quantity and decides what happens to the remaining amount based on the order type.

7. Event distribution

The engine sends execution events to the ledger, market data service, notification system, and reporting layer.

8. Order book update

Any remaining open quantity may stay in the order book, unless the order type requires cancellation.

Assume the best ask for BTC is $70,020 and a trader submits a buy order for 1 BTC at $70,020.

If only 0.6 BTC is available at that price, the matching engine executes 0.6 BTC first. The remaining 0.4 BTC may continue matching against the next available sell orders or remain open, depending on the order type.

From the trader’s screen, this may look like one simple action. Behind the scenes, the exchange must update locked balances, executed quantity, fees, trade history, order book depth, and market price data.

Many exchanges use a price-time priority model.

This means:

This rule creates a predictable execution process. It also provides a reason why the accuracy of a timestamp, sequencing of orders and controlling latency is important in exchange infrastructure. If a large number of orders are received at about the same time, the system should also be able to determine which order came first.

Low latency is a key requirement for a matching engine, however speed is not the only requirement. In a live trading environment, it is more important to be correct than to be fast.

A reliable matching engine must support:

The matching engine is the backbone of a crypto exchange. It’s not limited to matching buyers and sellers. It also controls execution logic, sequencing, partial fills, trade events, and system consistency.

For any serious exchange build, the goal is not just to build a fast matching engine. The goal is to build one that is fast, predictable, auditable, and tightly integrated with the ledger, order book, and market data infrastructure.

Liquidity is one of the primary factors that make a cryptocurrency exchange trustworthy or frustrating to deal with. A platform can have a great interface, assets listed, support wallets and a functional matching engine, but if users are unable to make trades at reasonable prices, then the exchange won’t be ready to trade seriously.

Crypto exchange liquidity refers to the availability of buy and sell orders for each trading pair. It is not only about high trading activity. What matters is whether the order book has enough active orders at fair price levels to support smooth execution.

A liquid exchange gives users more confidence that the price they see is close to the price they receive. When there is enough depth across bid and ask levels, trades can be matched without moving the market too much. This helps reduce slippage, improve execution quality, and make the platform feel more dependable.

Low liquidity creates a poor trading experience. The spread between the best buy price and best sell price may be wide. Larger trades may move through several price levels before they are fully filled. Some orders may only be partly completed, while others may take too long to execute.

To users, this feels like:

For example, if a trader wants to buy 10 BTC on a liquid exchange, there may be enough sell orders close to the current market price to complete most or all of the trade at a reasonable average price.

On an illiquid exchange, the same order may first consume the lowest-priced sell orders, then continue filling at higher price levels. The final average price becomes worse than expected. This price difference is known as slippage.

Liquidity should be planned before the exchange goes live. New exchanges often face a cold-start problem; traders do not want to trade on an empty order book, but the order book cannot grow without active traders.

Market makers help solve this by continuously placing buy and sell quotes. Liquidity providers and aggregators can also connect the exchange to external sources of market depth, especially during the early growth stage.

There is also a difference between internal and external liquidity. Internal liquidity comes from the exchange’s own users, institutional participants, or market-making activity. External liquidity comes from connected venues, brokers, aggregators, or liquidity networks. Many exchanges need both, depending on their target market, trading pairs, and expected order sizes.

For teams considering white label crypto exchange development, this is an important vendor discussion. The software may include a matching engine, wallet module, admin tools, and user interface, but liquidity is not automatically solved by the platform itself. The exchange still needs a clear liquidity model, partner strategy, and execution design.

| Liquidity Signal | What It Shows | Business Impact |

| Tight spread | Buy and sell prices are close | Users pay less to enter or exit trades |

| Deep order book | More orders exist across price levels | Larger trades execute with less price movement |

| Active market makers | Active market makersContinuous quotes support trading pairs | Markets feel more stable and usable |

| Low slippage | Expected and final prices are close | Traders trust the execution experience |

| Fast fills | Orders match quickly | Users are more likely to return |

Liquidity is not only a market feature. It affects pricing, trust, retention, and the technical design of the exchange.

A common misconception in the design of crypto exchanges is that what users see on the exchange is the same as what is in an on-chain wallet. In fact, these are linked systems, and not identical systems.

The exchange wallet infrastructure is responsible for blockchain-related activities. This includes deposit addresses, hot wallets for everyday deposits and withdrawal, cold wallets for long-term storage, multi-signature or MPC controls, withdrawal limits, workflows with approvals, and monitoring of the blockchain networks. These systems handle the movement of crypto assets on-chain.

Crypto custody refers to the ownership of private keys. For custodial exchanges, the platform is in charge of wallet infrastructure and key security for the users. Some exchanges run hybrid trading models in which trading is conducted off-chain but settlement and custodians are on-chain for speed.

The internal ledger is the exchange’s accounting layer. It records each user’s available balance, locked balance, deposits, withdrawals, trades, fees, rebates, settlement entries, and manual adjustments. This ledger must stay synchronized with the matching engine and wallet system.

For example, when a user places a buy order, the ledger should lock the required funds before the matching engine executes the trade. After execution, the ledger must update both the buyer’s and seller’s balances accurately. If this does not happen, the exchange may display incorrect balances, allow users to withdraw more than they own, or create financial exposure.

This is why strong crypto wallet development services should not only focus on wallets. They must also account for custody controls, ledger accuracy, reconciliation, and the operational rules that protect user funds.

Crypto exchange backend architecture is the system that makes the trading platform actually work as an integrated platform. It connects the user interface, trading engine, liquidity systems, ledgers, wallets, compliance checks and operator tools to ensure that all actions are validated, recorded and monitored.

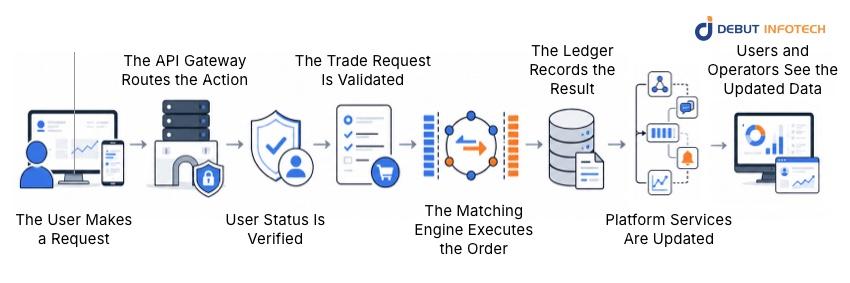

Typically, a practical exchange flow is of this nature:

The process begins on the frontend. A trader may log in, view market prices, place an order, check a balance, deposit crypto, or request a withdrawal.

The front-end only captures the action. The backend decides whether the action is allowed and how it should be processed.

The API gateway receives the request and sends it to the correct backend service. It also supports authentication, rate limiting, traffic control, access rules, and request filtering.

This prevents users or external systems from connecting directly to sensitive backend services.

Before the platform allows trading or fund movement, the backend checks the user’s session, account status, permissions, KYC level, and risk profile.

For example, a user may be able to view the BTC/USDT market but may not be able to trade or withdraw until verification is complete.

When an order is placed, the backend checks the trading pair, available balance, order size, price rules, account restrictions, and compliance requirements.

If the request passes these checks, it moves to the order book. If not, the system rejects it before execution.

The crypto exchange trading engine matches buy and sell orders based on the exchange’s matching rules. Once a match happens, the backend must update the trade status, lock or release funds, calculate fees, and prepare settlement records.

The internal ledger records every financial change. It tracks available balances, locked funds, trading fees, settlements, deposits, withdrawals, and transaction history.

For example, when a user sells BTC for USDT, the ledger must reduce BTC, credit USDT, apply the fee, and store a clear audit record.

After execution, event streams or message queues send the trade result to other systems, such as market data, wallet services, notifications, reporting dashboards, monitoring tools, and compliance review.

WebSockets update live prices, order books, and trade feeds. REST APIs support account history, balances, deposits, withdrawals, and settings. Admin tools give operators visibility into trades, risk events, wallet activity, and user actions.

That’s why digital asset exchange infrastructure needs to be unified into a coordinated back-end, not a disjointed set of tools. The platform must be able to execute trades swiftly, maintain a precise financial record, safeguard wallet transactions, identify operational problems, and provide administrators with transparent insights into all exchange activity.

The choice of a crypto exchange model should depend on the users the platform is addressing, the control level the platform is seeking for, and the level of infrastructure risks the business is willing to take. The table below provides you with a quick practical comparison of centralized, P2P, OTC, hybrid, and decentralized exchanges.

| Exchange Model | Core Trading Logic | Who Controls the Assets? | Best Fit | Main Backend Requirement | Main Risk to Manage |

| CEX | Orders are placed on a central order book and matched by the platform’s trading engine. | Usually the platform, through custodial wallets. | High-speed retail platforms, institutional exchanges, and broker-style trading apps. | Fast matching engine, internal ledger, custody system, KYC/AML workflows, and liquidity connections | Custody breach, compliance failure, downtime, and liquidity gaps. |

| DEX | Trades happen through smart contracts, liquidity pools, AMMs, or decentralized order books. | Usually the user, through connected wallets. | DeFi products, token trading platforms, and Web3 ecosystems. | Smart contracts, wallet integration, liquidity pool logic, oracle design, and blockchain settlement. | Smart contract bugs, low liquidity, network congestion, and gas cost issues. |

| P2P Exchange | Buyers and sellers trade directly, with the platform supporting escrow and dispute resolution. | Depends on escrow design; funds may be temporarily locked during the trade. | Fiat-to-crypto markets, local payment corridors, and regions with fragmented payment systems. | Escrow engine, payment verification, user reputation system, fraud checks, and dispute workflow. | Payment fraud, fake proof of payment, slow disputes, and weak user trust. |

| Hybrid Exchange | Uses centralized systems for speed while keeping some custody or settlement functions decentralized. | Shared between the user and the platform, depending on the design. | Platforms that want fast trading plus stronger user asset control. | Off-chain matching, on-chain settlement, wallet infrastructure, ledger synchronization, and risk monitoring. | Mismatched balances, delayed settlement, and complex system reconciliation. |

| OTC Desk | Large trades are handled privately through negotiated pricing and settlement arrangements. | Usually controlled through agreed custody, broker, or settlement arrangements. | Institutions, high-net-worth traders, treasury desks, and large-volume transactions. | Quote management, liquidity sourcing, counterparty checks, settlement tracking, and compliance records. | Counterparty failure, settlement delays, poor pricing visibility, and liquidity sourcing risk. |

For a business choosing between these models, the decision is less about the label and more about the operating burden. A CEX requires strong custody and compliance systems. A DEX depends on smart contract reliability and liquidity design. P2P platforms need fraud controls and escrow strength. Hybrid platforms add synchronization complexity, while OTC desks depend on private liquidity, settlement discipline, and counterparty trust. This is why decentralized exchange development has a very different infrastructure profile from building a custodial CEX or a fiat-focused P2P exchange.

A crypto exchange can’t fail just because of a broken user interface. Most serious failures happen behind the scenes, when the matching engine, ledger, wallet system, liquidity layer, market data feeds, compliance tools, and risk controls stop working in sync.

Poor infrastructure design can lead to the following problems:

| Failure Mode | What Happens | Business Impact |

| Weak matching engine | Orders are delayed, duplicated, partially filled incorrectly, or executed at the wrong price. | Traders lose confidence because execution quality is the core of the platform. |

| Poor liquidity planning | Order books are thin, spreads widen, and large trades suffer slippage. | Users move to exchanges with deeper markets and better pricing |

| Ledger mismatch | User balances do not match actual trades, deposits, or withdrawals | The platform faces financial, legal, and reputational risk |

| Wallet security gaps | Hot wallets are overexposed, private keys are poorly managed, or approval controls are weak | Asset loss, treasury risk, and possible platform shutdown |

For instance, when there is a high volume of trading, a trader could issue a market order. As your matching engine is slow, the liquidity layer is thin and the market data feed is delayed, the user could see one price and the other price would be executed. Even if it appears that the interface is still working, behind the scenes it has already failed the user.

The important thing to remember is that exchange infrastructure must be thought of as a connected system. All trading, custody, liquidity, compliance, settlement, reporting and reconciliation should be interconnected, with a continuous cycle. When one layer falls out of sync, the entire exchange becomes harder to trust.

If you’re considering selecting a vendor or beginning development, perform the following review to determine if your exchange is ready to plan architecture.

Build-Readiness Checklist

| Area | Key Questions to Confirm |

| Trading Infrastructure | Are matching engine requirements defined? Are order types confirmed?Are trading pairs and market data needs documented? Are latency and throughput targets clear? |

| Liquidity Readiness | Is the market-maker strategy defined?Have liquidity providers or aggregators been reviewed?Are order book depth, spreads, and slippage targets planned? |

| Wallet and Custody | Is the custody model selected?Are hot and cold wallet rules defined?Are MPC, multi-signature, and withdrawal controls reviewed? |

| Ledger and Settlement | Is the internal ledger design clear?Are available and locked balance rules mapped?Are fees, settlement, and reconciliation flows documented? |

| Compliance and Security | Are KYC and AML requirements identified?Are admin roles and permissions defined?Are audit logs, transaction monitoring, and incident response planned? |

For instance, when a user issues a limit order, the platform will place a “lock” on the funds, update the order book, complete the transaction, apply any transaction fees, and record the transaction for reconciliation.

If more than five items are not checked, the exchange is still at the concept level. Be sure to understand the infrastructure model before committing to your vendor, budget, or timeframe.

Talk with Debut Infotech’s exchange development team before the finalization of the architecture.

A crypto exchange works by connecting users who want to buy and sell digital assets through a trading system. In a centralized exchange, users deposit funds, place orders, and the exchange matches compatible buy and sell orders using an order book and matching engine. Once a trade executes, the internal ledger updates user balances, fees are recorded, and market data is broadcast across the platform. Deposits and withdrawals interact with blockchain networks, but most internal trading activity happens within the exchange’s own infrastructure.

The matching engine is the trading core of a crypto exchange. It compares buy and sell orders, applies matching rules such as price-time priority, executes trades, handles partial fills, and sends trade events to the ledger and market data systems. A strong matching engine must be fast, deterministic, fault-tolerant, and accurate because every execution affects real user balances.

Liquidity determines how easily users can buy or sell assets without causing major price movement. A liquid exchange has deep order books, tight spreads, active market makers, and enough volume across trading pairs. Poor liquidity leads to slippage, failed orders, wider spreads, and a trading experience that feels unreliable.

A cryptocurrency exchange processes trades by validating the user’s order, checking available balance, locking required funds, sending the order to the order book, and using the matching engine to find a compatible counterparty. When a match occurs, the system creates a trade event, updates buyer and seller balances in the ledger, applies fees, and updates market data. If the order is not fully matched, the remaining quantity may stay in the order book depending on the order type.

Cryptocurrency exchanges are powered by APIs, matching engines, order books, internal ledgers, wallet infrastructure, custody systems, risk engines, KYC/AML tools, databases, WebSocket market data feeds, and cloud or DevOps infrastructure. Centralized exchanges also require admin consoles, transaction monitoring, reporting tools, and security controls. More advanced platforms may include liquidity aggregation, market-maker integrations, institutional APIs, derivatives engines, and automated surveillance systems.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

9001:2015

Quality Certified

ISO 27001

Security Certified

A+ Rating

Accredited Business

Certik

Security & Audit

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy