ON THIS PAGE

Progress0%

Our Global Presence :

Does debt tokenization sound like another financial buzzword to you?

Let’s fix that!

It is a niche blockchain use case that only crypto aficionados should care about. A closer inspection reveals that it holds considerable potential for investors seeking the next big thing to invest in and generate real profits.

What’s more?

Most people are unaware of tokenized debt. If you ask any seasoned investor, they’ll tell you that the best investment opportunities are those that aren’t already saturated. Those who make the big bucks are early adopters who know how to spot real opportunities before others do.

If you think that is you, then this article was written with you in mind. Here you will find everything you need to know to begin your journey towards investing in debt tokenization. We cover benefits, risks, and limitations, key use cases, and lots more.

Let’s get into it!

Debt tokenization means converting traditional debt instruments, such as bonds and loans, into digital tokens on a blockchain.

Why would anyone want to do that?

On a basic level, these tokens are digital representations of rights, such as repayments, interest, or ownership. As such, tokenized debt ensures nobody gets cheated because they are embedded with smart contract rules that automate debt repayment processes.

On a more complex level, it extends beyond that. But we’ll get to that in a moment.

Debt tokenization has revolutionized credit, lending, and capital markets.

We know you’ve heard people say this often about new technology, but this time it’s really true.

Here’s how:

This process reduces reliance on intermediaries, shortens settlement cycles, and democratizes the financial market, allowing small players to share in the ‘big pie’. Additionally, it makes it easy to liquidate assets that were previously trapped in rigid, paper-based systems. These are some of the key reasons why you should consider debt tokenization.

Additional reasons are listed below:

Related Read: What is tokenization

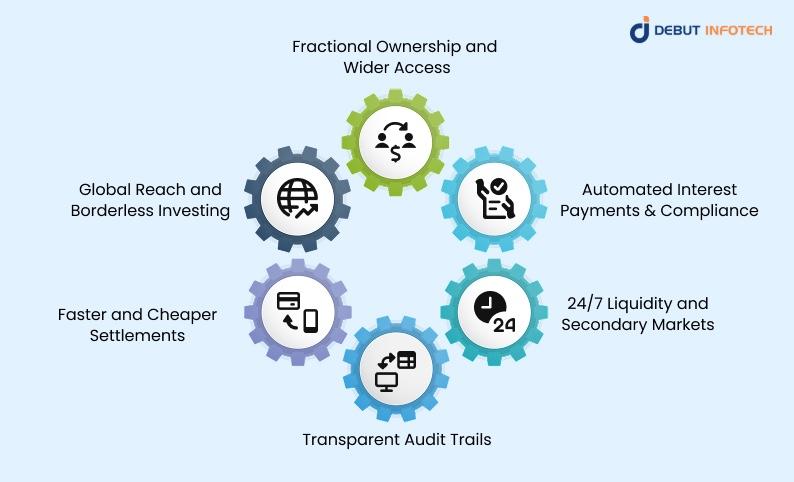

Debt tokenization provides a new layer of efficiency, accessibility, and automation in the world of finance. It does more than just digitize the old processes; it also makes them faster, more transparent, and opens up opportunities to investors across the globe—no gatekeeping.

Below are some of the most compelling benefits of debt tokenization.

Don’t have the big bucks necessary to invest in debts?

With debt tokenization, you don’t need to.

You can buy small units of a large debt instrument and still get a piece of the pie. This opens up the market to retail investors, students, freelancers, and others who were previously shut out by high minimum investment requirements.

Debt tokenization is executed by smart contracts.

This means that payments are processed once contract terms are met. By extension, this means that investors don’t have to be worried about missing deadlines or chasing their returns. It also helps issuers avoid administrative overhead since everything now operates automatically.

With debt tokenization, you can receive payments even before the debt reaches maturity. This represents a significant upgrade over the traditional debt system, where selling a bond before maturity is expensive, time-consuming, and sometimes impossible.

Debt tokenization also reduces the likelihood of fraudulent activities.

This is because every issuance, trade, payment, and ownership transfer is recorded on-chain, allowing everyone to see it. As a result, anyone (auditors, regulators, and investors) can verify transactions without relying on banks or third-party custodians. This transparency reduces the chances of fraud and increases trust.

Traditional debt systems require intermediaries, such as clearinghouses and custodians, to regulate the process. These intermediaries often charge a fee for their troubles.

Tokenized debts eliminate these intermediaries, thereby improving capital efficiency, reducing counterparty risk, and ensuring smoother cash flow for both issuers and investors.

With debt tokenization, you can invest in U.S. corporate debts, German municipal bonds, or African infrastructure projects from your phone—no need for international banking agreements. This makes cross-border investing simple, fast, and more affordable for everyone involved.

Debt tokenization sounds great on paper, but it’s not always a walk in the park.

However, a clear analysis of the risks and limitations equips you with the requisite knowledge you need to succeed in the debt game.

Below is a list of risks and limitations associated with tokenized debt.

Smart contracts are great, but they cannot compel a company to pay if it has insufficient funds.

Therefore, similar to traditional bonds, you could lose your principal or miss out on interest payments if the company defaults.

Tokenization doesn’t eliminate financial risks; it only changes the way obligations are enforced.

Debt tokenization is relatively new, so regulations are still in the early stages; some jurisdictions recognize them as legal securities, while others don’t. This legal uncertainty may make it difficult for you to recover your money if something goes wrong.

Smart contracts are code, and code can have bugs. Sometimes, hackers can exploit these bugs, and your funds could be lost, misdirected, or frozen.

It gets worse

Because smart contracts are immutable, bugs can’t be fixed unless explicitly allowed by the original code. This is a serious cause for concern.

If your debt tokens are stored on a centralized platform or in a custodial wallet, you could lose your tokens if that platform goes offline, gets hacked, or shuts down. That’s why you need expert advice on how to build a platform for tokenized debt so that you can consider all the requirements to mitigate platform or custody risks.

Decentralized protocols are safer but may carry risks if poorly managed or if they rely heavily on centralized infrastructure.

What if you can’t find a buyer when you want to sell?

That’s a possibility with Tokenized debt, especially if the market is thin or the asset is unpopular. This can reduce liquidity, and you may need to sell at a loss to recoup your investment.

If the debt is denominated in a volatile cryptocurrency or if the underlying project suffers reputational damage, token prices might fluctuate widely. This adds a speculative layer to what should be a fixed-income instrument. As such, many investors prefer debt tokens that are backed by fiat, stablecoins, or regulated entities.

Related Read: Tokenized Bonds in Fixed-Income Markets

Before you invest, it is essential to understand the distinction between the traditional debt system and the tokenized debt system. Having a clear understanding of the contrast between the two helps you appreciate what tokenization brings to the table.

Traditional finance has gone through centuries of improvement, with physical paperwork driving the industry. Debt instruments, such as bonds or promissory notes, have, over the years, involved a complex chain of brokers, custodians, clearinghouses, and legal oversight.

While this system is tested and trusted, it often suffers from numerous inefficiencies. For instance, transactions typically take days, with some taking several weeks.

Additionally, high administrative costs and high investment amounts frequently restrict opportunities to institutional players who can afford the entry barrier. This process, although legally robust, excludes retail investors with limited access or influence from participating in investment opportunities.

Tokenized debt instruments flip that model on its head.

Debt tokenization places debt instruments on the blockchain, thereby eliminating many of the problems associated with traditional debt systems.

Here are some ways it changes the debt process:

Related Read: Blockchain Use Cases Across Industries

The table below illustrates the differences between these two systems in key features, including accessibility, automation, liquidity, and compliance.

| Feature | Traditional Debt Instruments | Tokenized Debt Instruments |

| Minimum Investment Size | High entry barriers (e.g., $100k+) restrict participation to institutions | Fractional ownership enables participation with as little as $10 or $100 |

| Settlement Time | T+2 to T+5 days due to intermediary processes like clearinghouses and custodians | Near-instant (seconds to minutes) settlement via blockchain smart contracts |

| Transparency | Opaque records, limited to the issuer or custodians, often requiring audits | Fully transparent on-chain records are accessible in real time by all parties |

| Auditability | Requires manual audits and reconciliations; time-consuming and error-prone | Immutable, timestamped blockchain ledger simplifies auditing and compliance |

| Lifecycle Automation | Manual processing of coupons, principal repayment, and covenants | Automated cash flows, interest payments, and compliance via smart contracts |

| Global Reach | Constrained by local jurisdiction, time zones, and legal frameworks | Global issuance and trading 24/7 with fewer regulatory silos |

| Liquidity | Bonds and notes are traded on limited secondary markets with illiquidity discounts | Can be traded peer-to-peer or on decentralized exchanges, offering continuous liquidity |

| Custody and Record-Keeping | Typically handled by third-party custodians and transfer agents | Token wallets serve as self-custody systems, reducing fees and complexity |

Debt tokenization may sound futuristic, but many companies are already utilizing it to address long-standing issues in the financial sector.

Let us explore some of these use cases:

Tokenizing corporate bonds makes it possible for everyday investors to access high-value debt instruments while helping companies reduce their capital costs. This is particularly useful for startups and mid-sized firms looking for more sources of funding.

These offer several benefits, including:

Syndicated loans involve multiple banks co-lending to a single borrower. This process is often complex, slow-moving, and difficult to manage. Tokenization solves these problems by allowing investors to purchase programmable tokens that represent lender shares.

Here are some ways that debt tokenization improves syndicate loans

With tokenized debt, lenders can simply transfer their tokens on-chain, eliminating the need for lawyers to draft and sign assignment agreements. This shortens processing time, ensuring you can sell in a matter of minutes, not days.

Because smart contracts enforce debt tokenization, you don’t have to worry about errors or late payments—smart contracts calculate and distribute interest payments to token holders automatically, based on the amount they’ve invested.

Key performance metrics, covenants, and borrower activities can be monitored via integrated oracles that update the blockchain. This allows you to track borrower performance. As such, it improves risk management and facilitates immediate response when borrowers breach covenants

Inefficiencies, high costs, and credit risk plague the trade finance market. Tokenizing trade receivables transforms this multi-trillion-dollar market by enabling businesses to convert unpaid invoices into digital, liquid assets that can be sold to raise capital.

Here are some ways tokenization improves the trade finance market

Tokenization eliminates the need for intermediaries, allowing businesses to sell directly to investors on-chain within hours. This makes the process faster and allows companies to convert receivables without waiting for months for investors to settle their payments.

Tokenized municipal bonds can help local governments fund public projects more transparently and efficiently while working with local investors.

Debt tokenization allows residents of an area to buy low-denomination tokens to support community projects like schools, roads or utilities. This encourages citizens to be more involved in government. It also ensures that local investors can allocate their funds towards projects that matter to them.

With debt tokenization, governments can avoid relying on banks, underwriters, and costly bureaucracies. They can just issue debt directly to the public using user-friendly interfaces. Digital issuance platforms reduce reliance on banks, underwriters, and costly paperwork.

Goodbye to days of government misappropriation—with tokenization, you can track project milestones, fund allocation, and repayment schedules. This increases trust and accountability between citizens and governments. This helps to build a stronger social contract and better fiscal responsibility.

Securitization involves creating financial products that are bundles of different types of debt. Tokenization brings automation, transparency, and liquidity to a process that is typically manual and opaque.

Related Read: Tokenization vs Traditional Asset Management

Tokenized debt instruments are solving real-world problems by integrating blockchain technology into traditional debt systems. However, it comes with its unique challenges, particularly in terms of security.

To enjoy these benefits, you need to partner with a real world asset tokenization company that understands how to build a secure platform for tokenized debt. Debut Infotech Pvt Ltd has a wealth of experience building secure blockchain solutions with real-world applications. Contact us today to schedule a complimentary consultation with an expert.

A. Debt tokenization is the process of converting traditional debt instruments, such as loans and bonds, into digital tokens. This is done using Blockchain technology, which makes the process faster and more transparent.

A. The cost of tokenizing an asset or debt depends on the project’s size and a range of other project-specific criteria. As such, it can range from $5,000 and $50,000 to a much higher figure depending on the project requirements.

A. People who invest in debt tokens can sell them and make money from the sales. They could also wait for the debt to reach maturity and then receive payments in cryptocurrency or Fiat.

A. Smart contracts are codes that enforce the debt tokenization process. If they include bugs or faulty code, hackers may exploit it to steal funds.

A. Tokenization enables debt issuers to bypass intermediaries and transact directly with investors. This reduces administrative costs and also shortens transaction time. It also allows small investors to access investment opportunities.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy