ON THIS PAGE

Progress0%

Our Global Presence :

Stablecoin development in the U.S. is entering a new phase as Congress debates the GENIUS and CLARITY Acts. These laws aim to establish a stable regulatory foundation for stablecoins, thereby bridging fintech innovation and consumer protection.

As of early 2025, the U.S. dollar–pegged stablecoin market was valued at approximately $255 billion and processes over $15 billion in daily transactions, according to Defillama. At the same time, on-chain stablecoin transaction volume exceeded $8.9 trillion in the first half of 2025, according to CoinLaw. These figures reflect both rapid adoption and growing systemic importance. As regulation catches up to technology, U.S. stablecoin development is poised to evolve from speculative tokens into a core financial infrastructure.

In this guide, we will shed light on stablecoin development, the definitions of the GENIUS and CLARITY Acts, as well as their benefits, considerations, and challenges. We will also cover the impacts of the GENIUS and CLARITY Acts on stablecoin development and its future outlook.

Stablecoin development has become a central part of the U.S. digital asset ecosystem, bridging traditional finance and blockchain technology. These digital assets are designed to maintain price stability by being pegged to fiat currencies, such as the U.S. dollar. Developers, financial institutions, and regulators see stablecoins as critical infrastructure for payment systems, cross-border settlements, and tokenized assets. The broader focus is now shifting toward creating compliant, transparent, and scalable frameworks that ensure investor confidence and regulatory alignment.

By mid-2025, the U.S. contribution to global stablecoin circulation had exceeded $250 billion, with U.S. issuers accounting for nearly 99% of fiat-backed stablecoins, according to a report from MarketWatch. In addition, total stablecoin transaction volumes worldwide hit $4.6 trillion in H1 2025, across over one billion transactions, according to FXC Intel. This illustrates the growing importance of stablecoins in payments and money movement.

Large consumer brands are developing proprietary stablecoin solutions to streamline payments and loyalty integration. These branded coins could enable seamless checkout, instantaneous refunds, and reduced transaction fees. Over time, retailers may also use them to control consumer data and offer financial incentives tied to shopping behavior.

U.S. banks are piloting deposit accounts represented as stablecoin tokens, allowing real-time settlement and 24/7 availability. Tokenized deposits could shrink the gap between bank-led money and digital money. They also enable programmable features, such as conditional transfers and automated compliance checks, within the banking infrastructure.

Fintechs are using dollar-pegged stablecoins to bypass correspondent banking costs and delays. By converting local fiat to stablecoins, sending them across borders, and then converting back, they offer faster and cheaper remittances—especially into underserved corridors—while reducing foreign exchange spreads and settlement latency.

Global gig economy platforms are integrating stablecoin payments to compensate remote workers instantly and efficiently. This reduces dependency on local banks and swap fees and avoids delay in international wires. Freelancers can immediately convert to their local currency or hold stablecoins, offering flexibility and faster access to funds.

Merchants are experimenting with accepting stablecoins directly, sidestepping interchange and network fees. This shift also reduces chargeback risk and settlement latency. Payment systems built around stablecoins can interoperate with point-of-sale systems and digital wallets, facilitating smoother integration at scale.

Consumer brands are issuing loyalty stablecoins redeemable across partner networks and convertible to cash. These reward tokens run on blockchain infrastructure, enabling tradeable benefits, fractional rewards, and interoperability. Brands can thus deepen engagement, improve retention, and surface new monetization channels.

Related Read: How to Create a Stablecoin: Complete Guide

The Guaranteed Emergency and National Interest U.S. Stablecoin (GENIUS) Act is a proposed federal framework to regulate stablecoin issuance under the oversight of U.S. banking regulators. The Act mandates that stablecoin issuers maintain 1:1 reserves in U.S. dollars or equivalent short-term Treasury assets. Its objective is to ensure redemption security, prevent financial instability, and integrate stablecoin operations into the formal banking system.

Under the U.S. GENIUS Act, a fintech firm issuing a dollar-backed stablecoin would need to obtain a federal charter or partner with an insured depository institution. This setup enhances investor confidence, allows interoperability with banking rails, and ensures transparent reserve management through regular audits.

The GENIUS Act introduces clear guidelines for stablecoin issuers under federal oversight, replacing fragmented state-level rules. This unified framework enables developers, stablecoin development companies, and institutions to operate with confidence, thereby reducing legal uncertainty and promoting responsible innovation within the U.S. digital currency ecosystem.

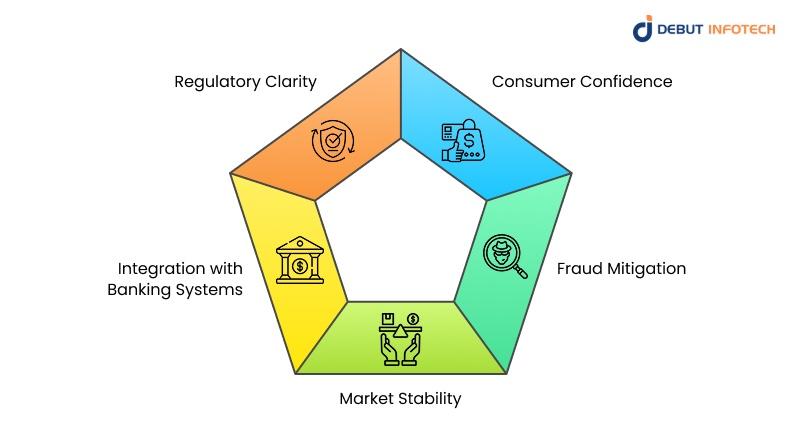

By mandating full 1:1 reserve backing in U.S. dollars or short-term Treasuries, the Act ensures that every issued stablecoin is fully redeemable. This transparency boosts user trust, minimizes redemption risk, and strengthens public confidence in the long-term stability of regulated digital assets.

The Act enables banks to issue or custody stablecoins within existing regulatory structures. This creates a seamless link between blockchain technology and traditional finance, allowing instant settlement, programmable payments, and interoperability across payment launchpad gateway networks without compromising regulatory compliance or deposit insurance coverage.

GENIUS requires independent audits, reserve verification, and strict reporting to federal agencies. These measures significantly reduce the risk of fraudulent activity, mismanagement, or reserve misrepresentation. Investors and consumers benefit from transparency that deters bad actors and strengthens the credibility of U.S.-backed stablecoins globally.

By enforcing stringent capital, liquidity, and redemption standards, the Act minimizes systemic risk associated with unregulated issuers. It aligns stablecoin operations with traditional financial safeguards, preventing sudden de-pegging events and ensuring market resilience during periods of volatility or liquidity stress.

Meeting GENIUS Act standards could impose heavy financial and operational burdens on smaller developers. Licensing, reserve audits, and legal consultations raise entry barriers, possibly consolidating the market under large financial institutions while limiting access for emerging fintech startups with innovative payment solutions.

The Act bans interest-bearing stablecoins to prevent them from functioning like unregulated securities. While this enhances consumer safety, it restricts innovation in decentralized finance (DeFi) and limits developers’ ability to design stablecoins with yield-generating mechanisms, stifling growth in on-chain lending and liquidity markets.

Stringent requirements may favor large banks and established fintechs, leading to reduced competition. Smaller issuers might struggle to comply with costly regulations, potentially concentrating stablecoin issuance within a few dominant entities. This could impact innovation, diversity, and slow the entry of new market participants.

Although designed to reduce instability, regulatory concentration under a few large issuers introduces a different form of systemic risk. A major operational failure or cyber incident involving a key regulated issuer could disrupt payment systems and trigger confidence shocks across the broader financial ecosystem.

Foreign stablecoin providers may face barriers to integrating with U.S. payment systems under the GENIUS framework. Disparate global regulations could limit cross-border interoperability, fragmenting liquidity pools and slowing international adoption of dollar-backed stablecoins that comply with U.S. federal standards.

Also Read: What are Stablecoins: Types, Functions, and Works

The Cryptocurrency Legal Accountability, Regulation, and Transparency (CLARITY) Act complements the GENIUS framework by defining digital asset classification and issuer responsibilities. It seeks to distinguish between payment stablecoins, investment tokens, and decentralized assets, bringing a consistent legal interpretation that fosters innovation without compromising consumer protection.

A decentralized payment platform operating under the CLARITY Act would need to disclose information about its token structure, governance, and reserve backing. This approach improves accountability while maintaining flexibility for innovation. Developers gain legal recognition for digital asset issuance without being automatically categorized as securities providers.

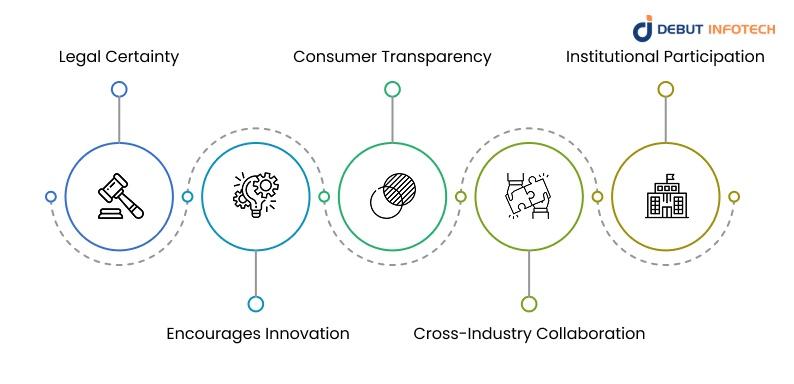

The CLARITY Act provides an explicit legal definition for stablecoins, distinguishing them from securities or commodities. This reduces regulatory ambiguity for developers and investors, protecting compliant issuers from arbitrary enforcement actions while ensuring stablecoins operate within a transparent, well-defined framework that supports innovation and accountability.

Developers gain freedom to experiment with compliant stablecoin designs without fear of misclassification. By offering clear guidance on registration and operational standards, the Act allows fintech startups to innovate safely, expanding blockchain-based payment, lending, and settlement solutions that align with U.S. consumer and financial regulations.

The Act mandates detailed public disclosures on reserve composition, governance mechanisms, and redemption procedures. Users can independently verify the stability and trustworthiness of a stablecoin, improving market discipline and confidence. This transparency discourages opaque practices, leading to a more secure and accountable digital asset environment.

The CLARITY Act creates a shared regulatory language between technology providers, banks, and regulators. By aligning compliance standards, it promotes partnership models that accelerate the institutional adoption of blockchain-based financial tools, streamlining communication between private issuers, regulators, and financial intermediaries within a unified framework.

Clear classification rules make it easier for traditional financial entities—such as banks, payment processors, and asset managers—to participate in U.S. stablecoin issuance or integration. The Act’s compliance-oriented structure reduces reputational risk, paving the way for large institutions to adopt blockchain solutions within a regulated financial environment.

Turning legislative intent into enforceable regulation will require extensive rulemaking across multiple agencies, including the SEC, CFTC, and Treasury. These overlapping jurisdictions may slow down implementation, causing uncertainty for issuers who are waiting for detailed compliance guidelines and operational requirements before launching or scaling stablecoin products.

Although designed to safeguard users, strict compliance obligations could unintentionally limit consumer choice. Smaller, decentralized projects may struggle to meet the costly disclosure or registration requirements, which can reduce the variety of available stablecoins and concentrate control among larger, better-funded issuers and institutions.

Applying anti–money laundering (AML) and know-your-customer (KYC) standards to decentralized ecosystems remains difficult. The Act’s compliance requirements may conflict with non-custodial or peer-to-peer models, forcing developers to redesign systems to meet identity verification rules without undermining decentralization or user privacy.

Stricter classification and compliance requirements could reshape market competition. Smaller issuers might withdraw due to regulatory costs, allowing major corporations and banks to dominate the stablecoin landscape. This concentration could stifle innovation and reduce diversity in use cases and technological experimentation.

The GENIUS and CLARITY Acts establish a unified legal framework for the issuance, operation, and redemption of stablecoins. Developers, financial institutions, and investors can now build compliant products without ambiguity over federal versus state oversight. This certainty promotes long-term planning, investor protection, and market expansion across the digital payment ecosystem.

Both Acts enforce strict reserve transparency, independent audits, and clear redemption mechanisms. These measures reduce fraud, ensure redemption at par value, and strengthen user trust in digital dollars. Consumers benefit from reliable, asset-backed stablecoins that operate within the safety of regulated financial systems, thereby reducing exposure to unstable or unverified projects.

The legislation opens a defined route for banks and payment providers to issue, hold, or distribute stablecoins under federal supervision. This formal bridge between traditional finance and blockchain infrastructure enables seamless integration of digital assets into mainstream banking, supporting real-time settlement and programmable finance capabilities across institutional platforms.

Clear rules foster an environment where startups can innovate without regulatory uncertainty. Fintech developers can now experiment with new payment models, tokenized savings systems, and cross-border applications built around stablecoins, knowing their frameworks comply with federal law. This alignment boosts investor confidence and encourages broader private-sector participation.

By guiding and establishing national transparent and enforceable standards, the Acts strengthen the U.S. position in the global stablecoin market. Regulatory clarity attracts foreign investment, supports international interoperability, and reinforces the dollar’s role in digital trade. This positions the United States as a leading jurisdiction for compliant, scalable innovation for U.S. Stablecoins Act.

The GENIUS and CLARITY Acts are expected to push stablecoins into mainstream finance by legitimizing their use across retail, banking, and institutional sectors. More businesses will issue branded digital dollars, and consumers may use them daily for remittances, payroll, and payments, driving real-world blockchain adoption.

As dollar-backed stablecoins gain trust globally under stronger U.S. oversight, the Acts could reinforce the dollar’s dominance in international settlements. Regulated digital dollars will likely replace offshore alternatives, ensuring greater U.S. influence in cross-border trade, global liquidity management, and financial system stability.

The framework sets a precedent for consistent U.S. stablecoin regulation that strikes a balance between innovation and investor protection. This clarity will reduce legal uncertainty for developers and issuers while simplifying compliance for institutions entering the market. Over time, it will help stabilize the regulatory environment for long-term blockchain growth.

These Acts could accelerate the broader tokenization of real-world assets. With a compliant stablecoin infrastructure in place, financial institutions can expand into tokenized assets, including bonds, real estate, and commodities. This evolution would deepen liquidity, enable fractional ownership, and push blockchain technology closer to mainstream financial integration.

The GENIUS and CLARITY Acts represent a significant milestone for stablecoin development in the United States. With clear oversight and capital requirements, stablecoin issuers can operate under transparent, federally supervised rules that strengthen market stability. These frameworks can enhance consumer trust and institutional adoption, while fostering innovation across payment systems.

Together, they aim to move stablecoins from loosely governed markets to a well-defined financial infrastructure that supports both digital asset growth and U.S. economic competitiveness.

Choosing a trusted development partner is vital for any business navigating the complex U.S. stablecoin regulatory landscape. Debut Infotech is a reliable, stablecoin development company that aligns every solution with evolving U.S. regulations. The company combines deep blockchain expertise with compliance-first design, ensuring secure, scalable, and regulation-ready stablecoin projects for startups, banks, and enterprises.

The GENIUS and CLARITY Acts are U.S. bills designed to give clear legal definitions for digital assets, including stablecoins. They aim to separate what constitutes a security from what doesn’t, helping stablecoin developers operate with fewer legal gray areas and greater regulatory consistency.

These Acts require stablecoin issuers to register with U.S. regulators, maintain full reserve backing, and adhere to strict transparency rules. Developers must ensure their tokens meet defined classifications, disclose audit reports, and prove that user funds are protected. Essentially, they advocate for accountability and transparent reserves.

Yes. Some argue the Acts could stifle innovation by adding too much red tape for smaller crypto projects. Others think they give too much power to regulators who may not fully understand blockchain tech. Still, many believe regulation is overdue to build public trust in stablecoins.

They need to register properly, document reserve holdings, and comply with disclosure and audit requirements. Working with legal experts on blockchain regulations is also a smart move. Staying proactive about compliance not only avoids penalties but also boosts credibility with investors, exchanges, and U.S. financial authorities.

Exchanges will likely have to tighten their listing rules. Only compliant stablecoins backed by verifiable reserves will make the cut. This could mean fewer options at first, but it’ll create a cleaner, more trustworthy market where users know the coins they trade meet regulatory standards.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy