ON THIS PAGE

Progress0%

Our Global Presence :

Tokenization is the new, shiny, and fancy term on the lips of anyone keeping up with finance trends.

While it has become cliche to use buzzwords like reducing cost and increasing efficiency, not many people know why.

In this article, we end by breaking down what tokenization brings to the evolving financial institution industry in terms of cost and efficiency.

What does modern-day tokenization finance have over the traditional finance system?

Here’s what we know so far:

Without further ado, let’s get into more details.

Tokenization in finance is the systematic process of creating digital representations of financial assets like stocks, bonds, loans, and accounts receivable that can be created on the blockchain to be traded securely in real time. These tokens are structured to reflect the fair value of the underlying financial assets, just like shares do.

The concept of tokenization finance institutions is poised to change the way nations trade while promoting a more inclusive financial participation across all sectors. But why is this the case?

What characteristics of tokenization make it easy for financial institutions to save cost and operate more efficiently?

Find out in the next section as we jump into 7 solid ways in which tokenization reduces cost and increases efficiency for financial institutions.

Tokenization in finance reduces the operational costs and boosts the efficiency of financial institutions in the following ways:

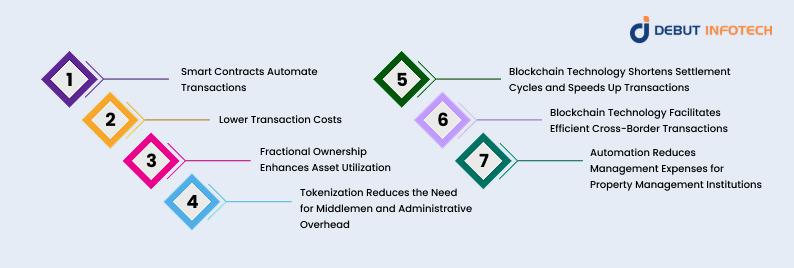

Smart contracts are automatically executed when the pre-defined conditions of asset transactions and management operations are met.

Let’s try to picture what typical transactions and management operations currently look like in a traditional financial institution.

So, investors deposit their funds manually, financial institutions handle the management processes by pushing documents online, and the same applies to documentation and record keeping.

There are more manual steps between all these, and that’s the point here: manual processes. This allows for errors and, more importantly, takes time.

With blockchain technology, smart contract developers only have to work with financial experts to decide the standard requirements, and they lock it in code once!

From that moment on, the smart contract handles everything automatically. For instance, common middle and back-office processes such as property sales, dividend distribution, and compliance checks can be automatically enforced and executed.

Still wondering why that is a good thing?

Projections by the Global Financial Markets Association estimate that automating these processes using smart contracts could result in operational cost savings of up to $15 – $20 billion. That’s pure upside for your financial institution!

It goes without saying that the costs associated with routine manual processes in financial services are one of the main factors driving up transaction costs. If a financial institution is paying less to handle day-to-day processes, it would be automatically incentivised to shift less financial burden to investors or customers.

Tokenization projects also rely on blockchain technology to reduce settlement times for processing trades. In traditional systems, different financial institutions use separate financial infrastructures and systems. This disparity is a major factor making it difficult and slow to reconcile inter-institution transactions.

However, blockchain technology unifies everyone involved, thus making it easy and cheaper to process each investor’s requests in record time.

Fractional ownership, a benefit of tokenization in finance, means that multiple investors can co-own assets or shares as opposed to only single entities. This increases the asset’s liquidity and makes it more accessible to more investors who probably have fewer resources.

However, it also helps save costs and increase a financial institution’s efficiency by enhancing asset utilization.

What does this mean?

Increased liquidity as a result of fractional ownership means that the financial institution can easily and efficiently convert the asset to cash without necessarily affecting its market price. This automatically means that financial institutions can spend less on holding and management costs to keep such an investment running smoothly.

After all, investors are easily paying cash for a piece of that asset right now. The overall return on investment automatically shoots up since the institution is spending less and the investors are still pumping more cash.

The same can’t be said of traditional approaches.

Eliminating middlemen and reducing administrative overhead is purely an efficiency gain, which also culminates in cost savings.

The truth is that most “large financial institutions” just have robust employee networks, with many individuals coming between the investors and the institution itself. As such, the investor incurs extra fees in “service charges” while the institution is leaving a lot of money on the table.

With tokenization, that robust infrastructure becomes lean yet productive. And did I mention fast?

An investor wants to get in on the action on a particular investor fund? Boom! They’re in under a few clicks.

Compared to the traditional way of going through different middlemen, this new infrastructure is quicker and more agile. And the institution doesn’t have to lose anything—well, except for the administrative overhead it has been incurring through its robust staff base.

The advantage here is that tokenized investments are more efficient and reliable when structured properly.

Financial institutions can be more efficient in terms of transaction speeds when they adopt tokenization and distributed ledger technology.

Traditional financial systems currently contain different individual technologies, which each institution adopts in-house. The downside is that the entire financial landscape lacks coherent atomic network connectivity. As a result, there’s a tendency for friction when processing transactions between institutions — I’m sure you’ve experienced those back-and-forths between different financial institutions.

So, what’s the alternative?

Tokenization introduces a new infrastructural backbone that reduces friction between financial institutions. Using the blockchain network, transactions become easy to process and approve. This bump in efficiency comes with a host of other benefits, such as increased liquidity, lower systemic risks, and greater market efficiency.

The involvement of multiple financial institutions and currency conversions in cross-border transactions hikes transaction costs. From currency conversions to complying with the different financial standards of the different regions, financial institutions undergo a lot when processing these transactions. As a result, these transactions often take days due to the involvement of these multiple institutions and time zone differences.

Alternatively, with tokenization, the entire process occurs on a centralized distributed ledger, thus effectively cutting out multiple intermediaries. Furthermore, most regions still have less strict or even non-existent regulations (in some regions) governing these cross-border transactions. Consequently, this speeds up the transaction time and reduces the associated transaction costs

Furthermore, the blockchain’s immutable ledger ensures transparency and security, with each transaction being verified and recorded in real time. This real-time verification further contributes to faster transaction speeds.

As a result, asset management and other financial institutions can facilitate cross-border transactions more efficiently

Financial institutions that manage properties often incur certain management costs to keep the property in top shape. For example, the property manager has to check in with the tenants, coordinate housekeeping efforts, collect rent, and perform a variety of other administrative tasks.

Not only do those activities cost money, but they also leave room for inefficiencies. For example, tenants may default on payments if they don’t get reminders, and even property managers may be sloppy with the entire thing.

But with blockchain technology, the entire process can become more efficient than ever before. Smart contracts can automate and enforce rent collection. They could also automatically update maintenance schedules, keeping all human agents on their toes at a fraction of the cost of property managers.

How’s that for boosting revenue?

Furthermore, the transparent and immutable nature of blockchain technology reduces the risk of fraud and disputes in this property management scenario. For instance, property managers don’t even have the opportunity to play fast and lose with rent collection records or property management bills because everything is recorded transparently on the blockchain’s distributed ledger network. Also, they are all automated by smart contracts. This lowers the need for expensive legal and dispute resolution processes.

All the signs are telling: The biggest financial institutions — Blackrock, JP Morgan Chase, BBVA, Ondo Finance, etc— are saving themselves a seat at the table.

Tokenization finance is already shaping up to represent a significant portion of modern-day financial institutions. And it’s not just a trend.

Tokenizing financial investments reduces costs and increases the efficiency of running a financial institution. If done right, both investors and institutions have a lot to gain. Start researching ways to get in on the action today.

Schedule a consultation with an asset tokenization development company like Debut Infotech Pvt Ltd for insights on how to get started with token development —it’s free!

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

9001:2015

Quality Certified

ISO 27001

Security Certified

A+ Rating

Accredited Business

Certik

Security & Audit

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy