ON THIS PAGE

Progress0%

Our Global Presence :

Decentralized Finance (DeFi) lending platforms have reshaped the traditional financial landscape by enabling permissionless access to loans, interest-bearing accounts, and asset lending, without relying on banks or intermediaries. As of early 2026, the total value locked (TVL) in DeFi protocols stands at approximately $128.6 billion, reflecting a significant presence in the financial ecosystem.

Leading platforms like Aave have achieved remarkable growth, with Aave’s TVL reaching $23.5 billion across multiple chains. At the same time, Compound maintains a substantial TVL of $2.08 billion, underscoring its role in the DeFi lending space. These platforms are integral to a broader financial ecosystem, attracting retail users and institutional players. DeFi lending offers greater transparency, operational efficiency, and accessibility, all powered by smart contracts that eliminate human inefficiencies and reduce transactional overhead.

So, there’s so much to gain from DeFi lending platforms in 2026. And in this guide, we’ll give you a quick rundown of the top 10 best DeFi lending platforms you should be looking into in 2026. Whether you’re looking to access deep liquidity or you’re a business looking to venture into DeFi lending and borrowing platform development, these 10 DeFi protocols are the best platforms to use in 2026.

A DeFi lending platform is a blockchain-based protocol that enables users to lend or borrow cryptocurrencies without relying on traditional financial intermediaries. These platforms use smart contracts to automate lending terms, manage collateral, and facilitate interest payments.

In contrast to conventional systems, DeFi crowdfunding platforms offer open access, meaning anyone with a digital wallet can participate. DeFi lending protocols remove geographic and institutional barriers, paving the way for a more inclusive financial ecosystem aligned with the decentralized vision of Web3.

You already know that DeFi lending is about connecting lenders and borrowers while bypassing banks or centralized intermediaries.

So, how is the connection established?

Two words: smart contracts!

For businesses exploring DeFi lending and borrowing platform development, this architecture offers transparency, automation, and global accessibility.

But how exactly does it work?

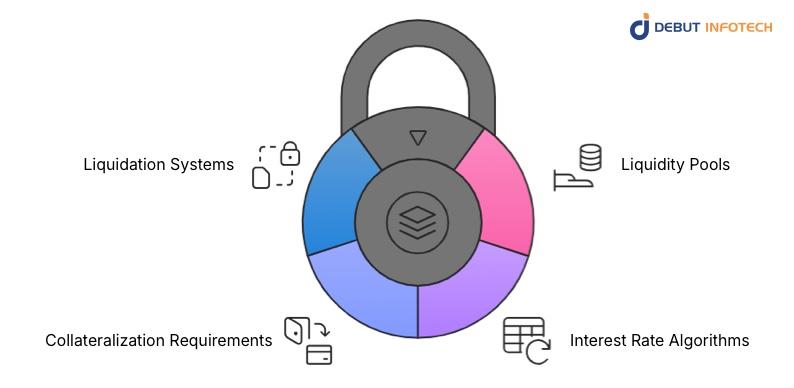

DeFi lending platform development involves the use of the concepts outlined below as the key mechanisms powering most DeFi lending platforms. They carefully explain how DeFi lending works.

Liquidity pools are collections of crypto tokens deposited by multiple participants and stored in smart contracts. Interested lenders deposit certain amounts of crypto assets into these shared pools for borrowers to be able to access or lend crypto assets when they want. In return, the lenders earn yield on their initial deposits whenever borrowers access the funds. This structure represent the base organisation for the best DeFi lending platform.

The interest rate algorithm is an automated process or step-by-step rules designed to adjust the interest rates of the loans that borrowers take out of the shared pool With this mechanism, the smart contracts containing the locked funds automatically adjust interest rates dynamically based on market utilization and other prevailing market conditions. In general, the principle behind these adjustments is that when demand for lending is high, interest rates spike, thereby incentivizing more deposits so borrowers can continue to have access to funds. On the other hand, low lending demand stabilizes interest rates.

Many DeFi platforms require borrowers to meet collateral requirements (usually a minimum amount of cryptocurrency) to access loans in shared pools. Each Borrowers typically post collateral worth 120–200% of the loan amount, enabling risk‑managed decentralized lending at scale.

These are automated, smart contract-driven mechanisms built into DeFi lending platforms to maintain solvency within the protocol. They do this by automatically selling the borrower’s collateral cryptocurrency whenever its value falls below a specific threshold.

The following are the top 10 best DeFi lending platforms you should consider in 2026 selected based on TVL, network footprint, protocol maturity, and institutional relevance.

| Platform | TVL (Approx.) | Primary Network(s) | Custody Model | Lending Architecture | Best Suited For | Launch Year |

| Aave | ~$26–27B | Ethereum + 10+ L2s | Non-custodial | Liquidity pool money market | Multi-chain enterprise lending | 2020 |

| Compound | ~$1.4B–$2B+ | Ethereum + select L2s | Non-custodial | Algorithmic rate protocol (cTokens) | Governance-driven lending builds | 2018 |

| Morpho Protocol | ~$5.8B | Ethereum, Base, Arbitrum, others | Non-custodial | Isolated market lending | Institutional & custom lending markets | 2022 |

| Kamino Finance | ~$1.8B–$2.1B | Solana | Non-custodial | Automated liquidity & credit markets | High-throughput Solana lending | 2024 (V2 era) |

| JustLend DAO | ~$6.0B–$7.6B+ | TRON | Non-custodial | DAO-governed liquidity pools | TRON-native DeFi lending | 2020 |

| Curve Finance (Lending) | ~$1.8B–$2.2B | Ethereum + L2s | Non-custodial | LLAMMA soft-liquidation lending | Stablecoin-focused borrowing | 2020 |

| Fluid (Instadapp) | ~$1.05B | Ethereum, Polygon, Arbitrum, Base | Non-custodial | Unified liquidity layer | Capital-efficient lending & DEX integration | 2023 |

| Binance Loans | Not Public | Centralized Exchange | Custodial (CeFi) | Crypto-collateralized exchange loans | Fast exchange-integrated borrowing | 2020 |

| Coinbase (via Morpho) | $1B+ originated | Base (Layer 2) | Hybrid (CeFi–DeFi) | On-chain lending via Morpho | Institutional crypto-backed loans | 2023 |

| Save Finance (Solend) | ~$1B peak | Solana | Non-custodial | Solana-native lending markets | High-speed DeFi lending on Solana | 2021 |

Total Value Locked: ~$26–27B across major networks

Supported Networks: 10+, including Ethereum, Arbitrum, Base, Avalanche, Polygon, Optimism, Metis, Gnosis, Scroll, BNB Chain

Launch Year: 2020 (originally ETHLend launched in 2017; rebranded to Aave in 2018)

Aave is an open-source protocol designed to serve as a non-custodial liquidity market for borrowers and lenders of all kinds. In 2026, it leads most other platforms in liquidity and usage, earning it a spot among the best DeFi lending platforms.

Furthermore, businesses seeking decentralized lending partnerships or looking to start developing DeFi lending and borrowing platforms often consider Aave due to its large, scalable infrastructure. In this money market protocol, there’s a multi-chain footprint that allows businesses like yours to deploy infrastructures scalably across both L1 and L2 ecosystems.

Pros:

Cons:

Total Value Locked: ~$1.4B–$2B+ across networks

Supported Networks: Ethereum, Arbitrum, Polygon, Base

Launch Year: 2018

Compound is an algorithmic interest rate DeFi lending protocol that was initially built to enable developers to access a wide range of open financial applications. Today, it has emerged as one of the most influential DeFi lending platforms due to its algorithmic interest rates and its novel cTokens. Both these innovative additions have played a significant tole in the modern decentralized lending ecosystem as we now see new DeFi lending platforms implementing variations of the same features.

You should consider using and partnering with Compound Protocol in 2026 because it has consistently proved reliable over the years in terms of sustained adoption. When it comes to DeFi lending and borrowing platform development, the Compound Protocol architecture remains highly commendable du to its COMP-powered governance model and transparent protocol evolution journey.

Pros:

Cons:

Total Value Locked: ~$5.8B

Supported Networks: Ethereum, Base, Arbitrum, Polygon, BNB Chain, OP Mainnet, Sei, Lisk, Etherlink, Unichain, Soneium (multi‑chain footprint)

Launch Year: 2022 (public launch + early fundraising milestones)

The Morpho Protocol is an open DeFi lending network connecting lenders and borrowers worldwide to the best financial opportunities. It is specifically designed for enterprises that require flexibility, risk controls, and modular infrastructure.

One feature that makes Morpho Protocol stand out is its isolated‑market architecture. This structure means that enterprises and institutions using the Morpho Protocol can customize their lending environments with parameters. Therefore, if you’re exploring the idea of developing a DeFi lending and borrowing platform, you might want to consider Morpho Protocol, particularly if you want thatlevel of customization. In the past year, Morpho has been integrating with other major platforms like Coinbase, Crypto.com, Gemini, Société Générale Forge, and Bitget, reinforcing its institutional positioning.

Pros:

Cons:

Total Value Locked: ~$1.8B–$2.1B

Supported Networks: Native to Solana (high‑speed, low‑cost environment)

Launch Context: Emerged as Solana’s leading lending protocol, evolving toward Kamino Lend V2 by 2024–2025.

Kamino Lend is an open-source, credit, and liquidity protocol built on Solana. It operates on a peer-to-peer system that unifies lending, borrowing, and leveraged-yield strategies. As such, it has become one of the fastest‑growing DeFi lending platforms on the Solana ecosystem. Its design focuses on automation, capital efficiency, and advanced liquidation engines.

As a result, enterprises seeking scalable decentralized lending infrastructure and high throughput often use Kamino Finance. Additionally, the protocol’s V2 upgrade introduces permissionless market creation. This engine is responsible for the growing awareness of the development of DeFi lending and borrowing platforms on Solana.

Pros:

Cons:

Total Value Locked: ~$6.0B–$7.6B+

Supported Network: TRON blockchain

Launch Context: First official lending platform on TRON

The JustLend DAO is the first official lending platform on TRON where users can borrow, lend, deposit assets, and earn interest. However, it has now grown into one of the largest DeFi lending platforms, serving as the backbone of TRON’s decentralized lending ecosystem. With billions in TVL and over 480,000 users, it offers businesses a highly active environment for decentralized lending applications and expansion into emerging markets.

Interest rates on the JustLend DAO are determined by market supply and demand, reflecting its non-custodial design and DAO governance model. As a result, users can borrow and lend TRX using different collaterals. At the same time, they can also stake Tron tokens with different APYs.

Pros:

Cons:

Total Value Locked: ~$1.8B–$2.2B

Supported Networks: Primarily Ethereum, with multi‑chain expansion across major L2s and EVM chains

Launch Context: Founded in 2020

Curve Finance is a decentralized exchange platform built specifically for stablecoin trading. However, it has a lending and borrowing unit that specializes in facilitating high-yield on-chain savings and protected borrowing, while covering both functions with low slippage. This lending and borrowing unit has now become one of the best DeFi lending platforms for 2026.

The Curve Finance Lending protocol operates using LLAMMA as its native liquidation mechanism. This mechanism facilitates a more capital-efficient decentralized lending by minimizing liquidation shocks and offering low fees for swapping. Therefore, this permissionless market creation and strong peg-stability mechanics are ideal features for any enterprise looking to enter the DeFi lending and borrowing platform development space.

Pros:

Cons:

Total Value Locked: ~$1.05B

Supported Networks: Ethereum, Polygon, Arbitrum, Base, etc.

Launch Context: Originally Instadapp; rebranded to Fluid with a unified liquidity‑layer vision.

Fluid is a cutting-edge DeFi protocol built by Instadapp for crypto users to lend, borrow, and trade cryptocurrencies without any hassle. As one of the most advanced DeFi lending platforms in 2026, Fluid operates as a liquidity layer that combines multiple functionalities, including lending, DEX trading, and collaterized borrowing, all on the same platform.

Decentralized lending on the Fluid platform has been further made efficient by features such as Smart Collateral, Smart Debt, and deep DEX integrations. Finally, and most importantly, Fluid has the qualities to make DeFi lending and borrowing platform development highly scalable for most institutions, as it minimizes liquidity fragmentation and supports high-LTV borrowing with minimal liquidation penalties.

Pros:

Cons:

Total Value Locked: Not publicly aggregated

Supported Networks: Centralized (CeFi) exchange with multi‑asset crypto collateral support, including BTC, ETH, USDT, and more.

Binance Loans offer a different flavor of DeFi lending platforms—CeFi‑based overcollateralized loans designed for users and institutions seeking fast, exchange‑integrated decentralized lending alternatives without interacting with on‑chain protocols. Borrowers can choose Flexible or Fixed‑Rate Loans, pledge a wide range of crypto assets, and access liquidity for trading, staking, or portfolio rebalancing. Binance supports isolated loan positions and real‑time LTV monitoring, making it operationally attractive for enterprises exploring DeFi lending and borrowing platform development, especially when building hybrid CeFi‑DeFi financial products.

Pros:

Cons:

Total Value Locked: Not disclosed, but Coinbase‑powered Morpho lending has surpassed $1B+ in originated on‑chain loans, with caps raised toward $5M per borrower.

Supported Networks: Loans operate on Base (Coinbase’s L2) using Morpho smart contracts; collateral includes BTC, ETH, XRP, DOGE, ADA, LTC and more.

Launch Context: Coinbase’s lending product is an interface that connects users to Morpho’s decentralized lending markets, combining CeFi trust with DeFi infrastructure.

Coinbase has emerged as a major institutional‑grade bridge into DeFi lending platforms, offering crypto‑backed USDC loans while relying on Morpho’s transparent on‑chain lending engine. Borrowers receive instant USDC with no fixed repayment schedule, while collateral is held on‑chain under Morpho’s isolated risk controls. This hybrid design makes Coinbase attractive for enterprises exploring DeFi lending and borrowing platform development but needing regulatory clarity, brand trust, and institutional UX. Coinbase’s expansion to support multiple collateral assets and higher borrowing caps highlights growing institutional demand for access to decentralized lending.

Pros:

Cons:

Total Value Locked: Historically peaked near $1B, now one of Solana’s largest lending protocols as part of its rebrand.

Supported Network: Solana (high‑speed, low‑fee lending infrastructure).

Launch Context: Originally launched as Solend (2021), rebranded to Save Finance in 2024 with expanded multi‑product DeFi offerings

Save Finance represents the evolution of Solana’s earliest and most battle‑tested DeFi lending platforms, expanding beyond borrowing and lending into a multi‑purpose ecosystem. The rebrand introduced three major products—SUSD, a 0%‑interest stablecoin; saveSOL, a liquid staking token; and dumpy.fun, a memecoin shorting app—positioning Save as a comprehensive decentralized lending and yield platform. For enterprises exploring DeFi lending and borrowing platform development, Save offers a high‑throughput Solana environment, redesigned UX, and broad collateral support, giving it strong potential for scalable user‑facing deployments.

Pros:

Cons:

DeFi lending has evolved into a powerful and maturing alternative to traditional finance. With smart contracts automating lending processes, users can instantly access deep liquidity and gain competitive returns on their investments, all while retaining full control over their assets.

Therefore, knowing the unique value propositions of platforms like Aave, MakerDAO, and Compound can help you if you’re looking for passive income as an individual or decentralized liquidity as an institution. As the industry adapts to tighter regulations, expands into real-world applications, and becomes more user-centric, the future of DeFi lending looks increasingly stable, scalable, and mainstream.

Therefore, to confidently participate in this growing financial frontier, you need to choose platforms that prioritize security, usability, and innovation.

While all these sound a bit too tricky as a first-timer, our DeFi development services at Debut Infotech Pvt Ltd are built to hold your hand through all the crucial decision-making process. Reach out to us today!

A. They open the door for anyone with an internet connection to borrow or lend—no credit checks, no banks judging you. It’s invaluable for people in places where traditional banking isn’t easy to access. DeFi basically gives more people a shot at managing their money.

A. With decentralized governance, users actually get a say in how the platform works, like voting on updates or rule changes. It can feel empowering, but also a bit chaotic if too many cooks are in the kitchen. Still, it beats decisions coming from just one company.

A. Yield farming lets users earn extra crypto by lending or staking their assets. It’s kinda like putting your money to work 24/7. The rewards can be pretty decent, though it’s not risk-free. Rates change fast, and if the market dips, your earnings might too.

A. No banks, no middlemen, and no paperwork. Everything runs on code. You can lend or borrow in minutes, usually with better rates. It’s faster, more transparent, and often cheaper—but you’ve got to be more hands-on and know what you’re doing. No hand-holding here.

A. Smart contracts are the brains behind DeFi lending. They handle everything—from loans to repayments—automatically and without bias. No need to trust a person or a company; you trust the code. Of course, if that code has bugs, well… that’s a whole different problem.

Our Latest Insights

USA

2501 Chatham, Rd Suite R Springfield, IL 62704

+1-708-515-4004

info@debutinfotech.com

UK

7 Pound Close, Yarnton, Oxfordshire, OX51QG

+44-770-304-0079

info@debutinfotech.com

Canada

154 Eden Oak Trail, Kitchener, ON N2A 0H9

+1-708-515-4004

info@debutinfotech.com

INDIA

Sector 101-A, Plot No: I-42, IT City Rd, JLPL Industrial Area, Mohali, PB 140306

9888402396

info@debutinfotech.com

Copyright © 2026, Debut Infotech. All rights reserved. | Privacy Policy